Government Shutdown Set to End as Markets Rally on Policy Clarity | Links: [1], [2], [3]

The longest US government shutdown in history appears set to conclude, with the Dow notching a record high close as traders positioned for resumption of normal government operations. Asian markets advanced overnight as political uncertainty began to lift, creating a more predictable environment for global asset allocation decisions. The shutdown's resolution will restore crucial economic data releases that have been delayed for weeks, including jobs and inflation reports that markets desperately need for Fed policy assessment. White House officials project aggressive 3-4% economic growth by early 2026 despite the shutdown's temporary drag, expressing confidence in policy initiatives including potential dividend payments and housing measures. Historically, the combination of removed political uncertainty and restored data flow has reduced volatility premiums and supported equity strength, though delayed data releases could create temporary volatility spikes once published.

Weak Labour Data Drives Central Bank Easing Bets Across Atlantic | Links: [4], [5], [6]

Deteriorating employment conditions on both sides of the Atlantic have dramatically shifted monetary policy expectations, with UK unemployment surging to 5.0% - the highest since the pandemic - while US payrolls weakness drove Treasury rallies. UK wage growth cooled substantially as unemployment jumped from 4.8%, prompting JPMorgan to back a December Bank of England rate cut as market pricing for such a move soared to 75%. The FTSE 100 hit record highs on these rate cut bets, while sterling snapped a four-day winning streak. In the US, softer jobs data strengthened December Fed cut expectations, contributing to a broader bond rally as traders positioned for more accommodative policy. The synchronised labour market softening across major economies suggests global growth concerns are mounting despite recent market strength, creating increased easing expectations that support fixed income across the Atlantic whilst generating currency volatility.

European Markets Hit Records Despite ECB Policy Confidence | Links: [7], [8], [9]

European equities defied global growth concerns by closing at record highs, with the STOXX 600 reaching new peaks led by healthcare shares and optimism about reduced US political uncertainty. This strength occurred even as ECB policymakers expressed growing confidence in their inflation and growth outlook, indicating potential divergence from the dovish pivot seen in the UK and US. German investor morale unexpectedly declined in November according to ZEW data, yet European markets continued their advance supported by expectations that the region's lower technology exposure shields it from AI investment concerns plaguing US markets. The Bank of France maintained an optimistic economic expansion outlook despite ongoing political risks, reinforcing the narrative that European markets may offer relative value compared to stretched US valuations. This European market strength creates rotation opportunities from expensive US assets while ECB policy divergence may provide euro support.

SoftBank's $5.8bn Nvidia Exit Stirs AI Bubble Concerns | Links: [10], [11], [12]

SoftBank's complete disposal of its Nvidia stake for $5.8 billion sent shockwaves through technology markets, with SoftBank shares plunging as much as 10% in Tokyo trading. The timing of the sale, coinciding with the $500 billion Stargate AI infrastructure project announcement, indicates major capital reallocation within the tech ecosystem rather than loss of faith in AI fundamentals. However, the move amplifies existing concerns about AI investment returns, with 'Big Short' investor Michael Burry separately accusing AI hyperscalers of artificially boosting earnings through questionable accounting practices. Adding to the technology sector's woes, fund concentration limits are preventing managers with $100 billion in assets from reducing TSMC exposure, highlighting systemic risks in mega-cap tech positioning. The combination of high-profile profit-taking and valuation scrutiny is creating headwinds for a sector that has powered much of 2024's market gains, pointing to near-term consolidation despite the AI investment theme remaining intact.

Emerging Markets Attract $27 Billion October Inflow | Links: [13]

Foreign investors added $27 billion to emerging market portfolios in October, marking one of the strongest monthly inflows in recent years as global risk appetite shifted toward developing market assets. Equity inflows led the charge across Asia, Latin America, and Europe, with the broad-based appetite indicating improving sentiment toward EM assets amid expectations of more accommodative global monetary policy. The shift toward EM equity over debt demonstrates growth optimism is outweighing yield-seeking behaviour, as investors position for potential outperformance from markets that have lagged developed counterparts. This capital reallocation reflects institutional recognition that emerging markets may offer better risk-adjusted returns as developed market valuations stretch to extreme levels and central bank policy becomes more supportive globally. The strong inflows support currencies and equity valuations across developing markets while creating tactical opportunities for managers seeking value outside expensive developed market assets.

| S&P 500 | 6846.61+30.97▲ +0.45% |

| FTSE 100 | 9899.60+112.40▲ +1.15% |

| CAC 40 | 8156.23+75.63▲ +0.94% |

| DAX 40 | 24088.10+98.00▲ +0.41% |

| Dow Jones | 47928.00+543.50▲ +1.15% |

| Euro Stoxx 50 | 5725.70+54.76▲ +0.97% |

| Hang Seng | 26696.40-51.70▼ -0.19% |

| Nasdaq 100 | 25533.50+32.60▲ +0.13% |

| Nasdaq Comp | 23468.30+60.60▲ +0.26% |

| Nikkei 225 | 50842.90-471.10▼ -0.92% |

| S&P/ASX 200 | 8818.80-17.10▼ -0.19% |

| Shanghai Comp | 4002.76-21.12▼ -0.52% |

| S&P 500 E-mini | 6882.25+10.75▲ +0.16% |

| Nasdaq 100 | 25721.50+80.75▲ +0.31% |

| FTSE 100 | 9936.00-1.50▼ -0.02% |

| Euro Stoxx 50 | 5751.00+16.00▲ +0.28% |

| WTI Crude | 60.84-0.20▼ -0.33% |

| Gold | 4115.10-1.20▼ -0.03% |

| Copper | 5.04-0.02▼ -0.48% |

| US 10Y Treasury | 112.91-0.12▼ -0.11% |

| UK 10Y Gilt | 118.11-0.02▼ -0.02% |

| German 10Y Bund | 129.21-0.02▼ -0.02% |

| Italian 10Y BTP | 121.34+0.08▲ +0.07% |

| US Dollar Index | 99.46+0.14▲ +0.14% |

| VIX Volatility | 19.25+0.00▲ +0.03% |

| SONIA 3M | 96.28+0.04▲ +0.04% |

• German Wholesale Prices MoM at 07:00 GMT - Forecast: 0.1% vs Previous: 0.2% - Indicates easing inflationary pressures in Europe's largest economy, potentially influencing ECB policy expectations and EUR strength.

• Chinese New Yuan Loans at 08:30 GMT - Forecast: ¥500.0B vs Previous: ¥1290.0B - Sharp decline in credit creation could signal tightening monetary conditions and weaker domestic demand, impacting commodity markets and China-exposed equities.

• Italian Industrial Production MoM at 09:00 GMT - Forecast: 1.5% vs Previous: -2.4% - Expected recovery from sharp contraction could boost confidence in eurozone manufacturing recovery and support European equity sectors.

• Indian Inflation Rate YoY at 10:30 GMT - Forecast: 0.48% vs Previous: 1.54% - Further decline in inflation may provide RBI room for more accommodative policy, potentially strengthening INR and emerging market sentiment.

• UK BoE Pill Speech at 12:05 GMT - Deputy Governor's remarks could provide insights into BoE's policy stance amid evolving inflation dynamics, directly impacting GBP and UK gilt yields.

• US Fed Williams Speech at 14:20 GMT - New York Fed President's comments on monetary policy outlook will be closely watched for clues on future rate path, influencing USD and Treasury markets.

• Hon Hai Precision Industry Co., Ltd. (2317) at 12:00 GMT [Pre-Market] - Est: $0.12 vs Prev: $0.11 - Major Apple supplier's results will signal health of global electronics supply chain and consumer device demand.

• Transdigm Group Inc. (TDG) at 12:15 GMT [Pre-Market] - Est: $10.04 vs Prev: $9.60 - Aerospace parts supplier's performance indicates commercial aviation recovery momentum and defense spending trends.

• Cisco Systems, Inc. (CSCO) at 21:05 GMT [After-Hours] - Est: $0.98 vs Prev: $0.99 - Networking giant's guidance will reveal enterprise IT spending patterns and AI infrastructure investment demand.

• Manulife Financial Corporation (MFC) at 21:00 GMT [After-Hours] - Est: $0.75 vs Prev: $0.70 - Canadian insurer's results reflect interest rate environment impact on financial sector profitability.

• Infineon Technologies AG (IFX) at 06:30 GMT [Pre-Market] - Est: $0.51 vs Prev: $0.44 - German semiconductor leader's outlook will indicate automotive chip demand and industrial automation trends.

• Loblaw Companies Limited (L) at 11:30 GMT [Pre-Market] - Est: $0.49 vs Prev: $0.44 - Canada's largest grocer provides insight into consumer spending resilience amid inflationary pressures.

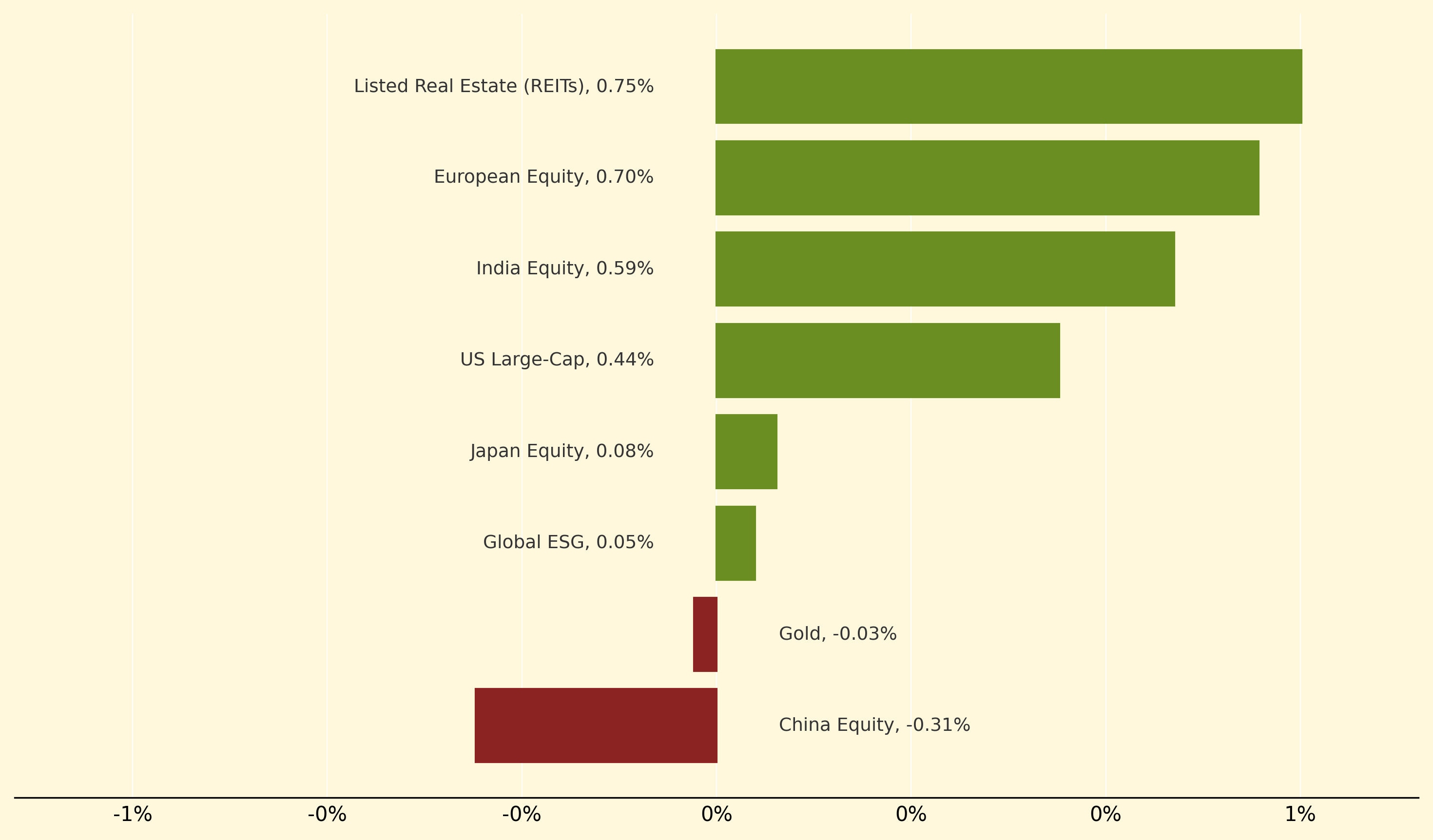

Listed Real Estate (REITs) topped performance with a 0.75% gain, benefiting from rate cut expectations following weak labour data across major economies, as lower rates typically boost property valuations. European Equity also advanced strongly at 0.70%, reflecting the STOXX 600's record highs driven by healthcare strength and reduced US political uncertainty as the government shutdown nears resolution.

China Equity underperformed, declining 0.31% as the only strategy posting meaningful losses, highlighting ongoing concerns about economic challenges despite the central bank's commitment to accommodative policy. Gold's marginal 0.03% decline indicates muted safe-haven demand as political clarity emerged, while other "losing" strategies like Global ESG and Japan Equity actually posted small gains, demonstrating the market's generally positive tone.

Volatility premiums: Additional pricing built into options and derivatives to compensate for expected price swings during uncertain periods. These premiums typically spike during political or economic uncertainty, then compress as clarity returns, directly affecting trading costs and market efficiency across asset classes.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry