Global Markets Rally on Trump-Xi Trade Optimism | Links: [1], [2], [3], [4], [5]

Wall Street and European indices scaled fresh record highs yesterday as investors positioned for a potential breakthrough in US-China trade relations ahead of direct talks between Trump and Xi Jinping this week. The Shanghai Composite broke above its 10-year trading range for the first time since 2014, signalling renewed confidence in Chinese markets as Trump suggested the two nations were "close to a trade deal" that could address his 100% tariff threat on Chinese goods. Soybeans extended gains in anticipation of agricultural trade resumption, while the dollar softened amid expectations of reduced trade tensions. The synchronised rally reflects market anticipation of a shift from confrontation to cooperation between the world's two largest economies, with potential implications for global supply chains and commodity flows.

Fed Rate Cut Expected Amid Major Central Bank Week | Links: [6], [7], [8]

The Federal Reserve appears likely to deliver a quarter-point rate cut this week, with markets increasingly pricing in further easing ahead as the central bank prepares to end its quantitative tightening programme. A large rates market trade worth $2-3 billion positions for the conclusion of the Fed's balance sheet unwind and potential liquidity backstops, indicating expectations of significant policy shifts. Bond investors have scaled back longer-dated Treasury positions ahead of the meeting, anticipating dovish signals that could prove bullish for the broader Treasury market. The Fed's decision comes amid a week of coordinated central bank meetings, with the ECB expected to hold rates steady and the Bank of Japan likely to maintain its accommodative stance, creating currency market volatility as the dollar weakens ahead of the Fed's dovish pivot.

Big Tech Earnings Face AI Bubble Scrutiny | Links: [9], [10], [11]

Major technology companies report earnings this week under intense examination over whether their large AI infrastructure investments, totalling $400 billion across the sector, are generating sustainable returns or creating a speculative bubble reminiscent of the dotcom era. The 'Magnificent Seven' tech giants face particular focus as investors seek evidence that AI spending can translate into revenue growth rather than circular deals between cloud providers, with concerns mounting over debt-financed AI infrastructure projects. Qualcomm's announcement of new AI chips to compete directly with Nvidia and AMD triggered an 11% surge in its stock price, highlighting intensifying competition in the AI semiconductor space. However, Amazon's announcement of its largest-ever corporate layoffs, potentially affecting up to 30,000 employees, adds to questions about whether tech companies are rightsizing after years of AI-driven expansion.

Russian Energy Sanctions Reshape Global Oil Flows | Links: [12], [13], [14], [15]

New US sanctions on Russian energy are forcing major adjustments in global oil trade patterns, with Indian refiners - who process 40% of Russia's oil exports - pausing new orders while awaiting clarity on compliance requirements. Key Russian oil grades are experiencing sharp price declines as Chinese buyers also scale back purchases to avoid sanctions risk, while European refiners respond by ramping up diesel and jet fuel imports to record levels in anticipation of supply disruptions. The sanctions are creating a complex web of supply chain adjustments, with Lukoil announcing plans to divest its international assets to navigate the new restrictions. However, the IEA suggests that global surplus capacity may limit the overall impact on oil prices, with the market remaining in a relatively stable $60-65 range despite mounting geopolitical pressures.

BIS Warns on Private Loan Credit Rating Inflation | Links: [16]

The Bank for International Settlements has issued a stark warning that private loan credit ratings may be 'systematically' inflated, raising serious concerns about institutional investors' exposure to these increasingly popular instruments. The warning highlights potential fire sale risks if these credit assets face sudden repricing, particularly given the massive growth in private credit markets over the past decade and rating agencies potentially applying more lenient criteria compared to publicly traded debt. With pension funds, insurance companies and sovereign wealth funds having significantly increased their allocations to private credit seeking higher yields, any systematic repricing could trigger broader market instability. The timing proves particularly significant as credit markets rally alongside equities, potentially masking underlying risks in the current risk-on environment that could force investors to reassess their private credit exposure and risk management frameworks.

| S&P 500 | 6875.16+29.70▲ +0.43% |

| FTSE 100 | 9653.80+8.20▲ +0.09% |

| CAC 40 | 8239.18+1.98▲ +0.02% |

| DAX 40 | 24308.80-24.00▼ -0.10% |

| Dow Jones | 47544.60+131.80▲ +0.28% |

| Euro Stoxx 50 | 5711.06+19.17▲ +0.34% |

| Hang Seng | 26433.70-62.30▼ -0.24% |

| Nasdaq 100 | 25821.60+119.70▲ +0.47% |

| Nasdaq Comp | 23637.50+100.20▲ +0.43% |

| Nikkei 225 | 50512.30+606.50▲ +1.22% |

| S&P/ASX 200 | 9055.60+36.60▲ +0.41% |

| Shanghai Comp | 3996.95+27.73▲ +0.70% |

| S&P 500 E-mini | 6903.75-4.50▼ -0.07% |

| Nasdaq 100 | 25954.20-9.50▼ -0.04% |

| FTSE 100 | 9690.50+8.00▲ +0.08% |

| Euro Stoxx 50 | 5706.00-11.00▼ -0.19% |

| WTI Crude | 61.13-0.18▼ -0.29% |

| Gold | 3988.80-30.90▼ -0.77% |

| Copper | 5.14-0.03▼ -0.63% |

| US 10Y Treasury | 113.50+0.08▲ +0.07% |

| UK 10Y Gilt | 118.29+0.01▲ +0.01% |

| German 10Y Bund | 129.63+0.06▲ +0.05% |

| Italian 10Y BTP | 121.36+0.20▲ +0.17% |

| US Dollar Index | 98.36-0.25▼ -0.26% |

| VIX Volatility | 18.11+0.08▲ +0.42% |

| SONIA 3M | 96.24-0.01▼ -0.01% |

• German GfK Consumer Confidence at 07:00 GMT - Forecast: -22.0 vs Previous: -22.3 - Key gauge of eurozone's largest economy's consumer sentiment, influencing ECB policy expectations and EUR strength.

• Italian Business Confidence at 09:00 GMT - Previous: 87.3 - Critical measure of eurozone's third-largest economy's corporate outlook, affecting European equity markets and regional growth projections.

• Italian Consumer Confidence at 09:00 GMT - Previous: 96.8 - Reflects household spending power in major eurozone economy, impacting retail sector performance and domestic demand forecasts.

• Indian Manufacturing Production YoY at 10:30 GMT - Previous: 3.8% - Indicates industrial strength in world's fastest-growing major economy, influencing emerging market sentiment and INR volatility.

• Indian Industrial Production YoY at 10:30 GMT - Previous: 4.0% - Broader measure of India's economic momentum, affecting global growth outlook and commodity demand expectations.

• South Korean Business Confidence at 21:00 GMT - Previous: 70.0 - Signals corporate sentiment in key Asian economy and tech hub, impacting regional markets and semiconductor sector outlook.

• Iberdrola SA (IBE) at 07:00 GMT [Pre-Market] - Est: $0.25 vs Prev: $0.27 - European utility earnings could signal renewable energy investment trends and impact broader clean energy sector sentiment.

• UnitedHealth Group Incorporated (UNH) at 09:55 GMT [Pre-Market] - Est: $2.80 vs Prev: $4.08 - Healthcare sector bellwether's guidance on medical costs and Medicare Advantage growth will influence healthcare stock valuations.

• Novartis AG (NOVN) at 12:00 GMT [Pre-Market] - Est: $2.27 vs Prev: $2.42 - Swiss pharma giant's pipeline updates and biosimilar competition commentary could move European healthcare indices.

• NextEra Energy, Inc. (NEE) at 13:30 GMT [During-Hours] - Est: $1.04 vs Prev: $1.05 - Leading US utility's renewable capacity additions and rate base growth outlook will impact clean energy infrastructure investments.

• Visa Inc. (V) at 20:00 GMT [During-Hours] - Est: $2.97 vs Prev: $2.98 - Payment processing volumes and cross-border transaction trends will signal global economic activity strength.

• Booking Holdings Inc. (BKNG) at 20:00 GMT [During-Hours] - Est: $95.70 vs Prev: $55.40 - Travel demand indicators and international booking trends could influence broader leisure and hospitality sector performance.

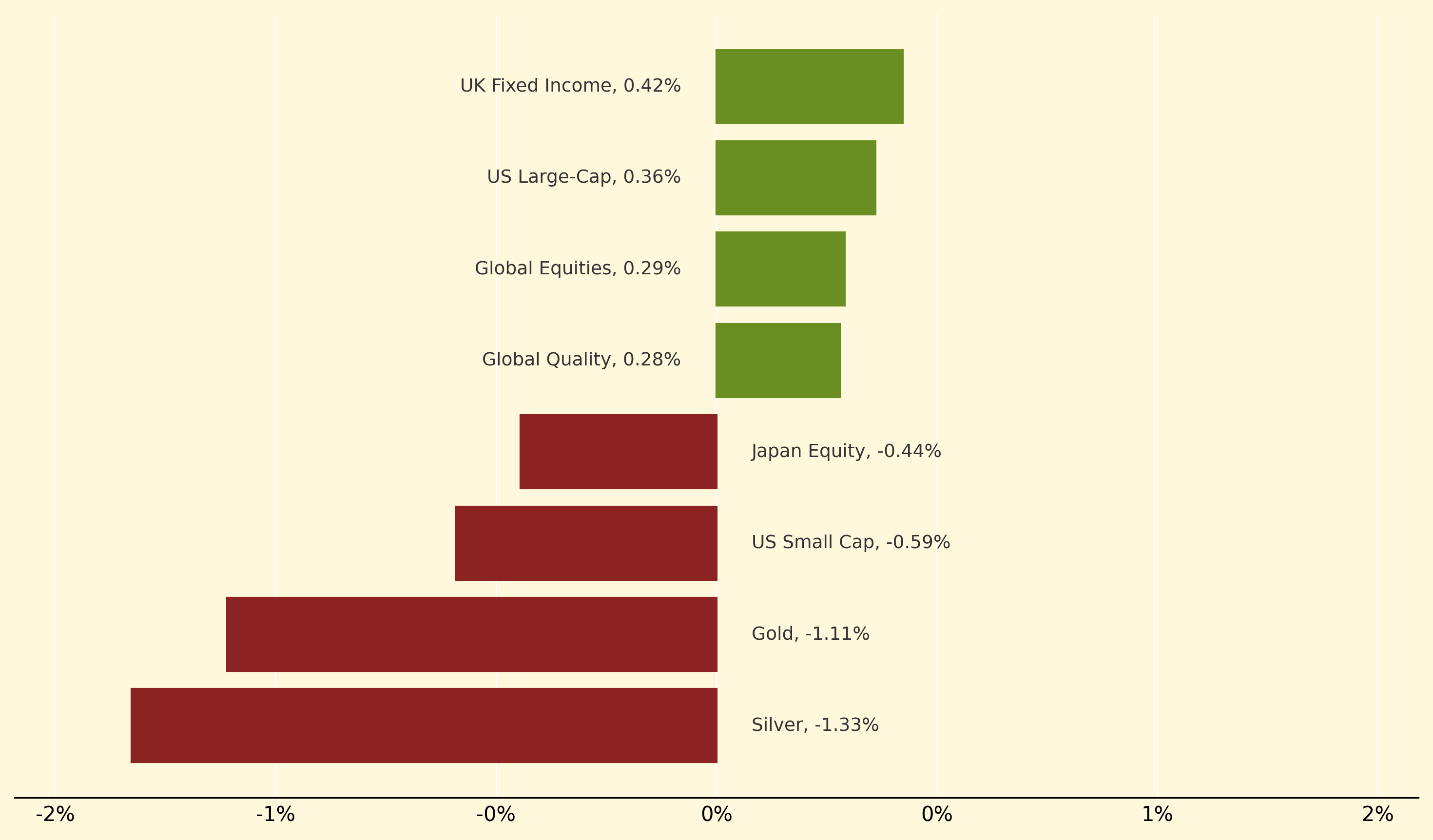

UK Fixed Income topped the winners, climbing 0.42% as expectations of Fed rate cuts and reduced trade tensions supported bond markets amid the broader risk-on rally. US Large-Cap equities also performed strongly, advancing 0.36% alongside Global Equities (0.29%) as investors positioned for potential US-China trade breakthroughs ahead of Trump-Xi talks.

Precious metals faced significant pressure, with Silver plummeting 1.33% and Gold dropping 1.11% as trade optimism and softer dollar expectations reduced demand for safe-haven assets. Small-cap strategies also lagged, with US Small Cap falling 0.59% and Global Small Cap declining 0.30%, suggesting investors favoured larger, more established companies amid the shifting macro environment.

Quantitative tightening: The Federal Reserve's process of reducing its balance sheet by allowing bonds to mature without replacement, effectively removing liquidity from the financial system. Markets closely monitor QT programmes as they can influence Treasury yields, bank reserves, and overall market liquidity conditions.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry