IMF Sounds Triple Warning on Global Financial Stability Risks | Links: [1], [2], [3]

The International Monetary Fund has issued its most severe warning on global financial stability in months, raising concerns across three critical fronts. Risk assets are trading "well above fundamentals" with increasing odds of a "disorderly" global market correction, while the Fund highlights dangerous interconnectedness between traditional banks and the $4.5 trillion shadow banking sector. The AI boom, meanwhile, poses "a key risk" to an increasingly volatile global economy. These warnings accompany the IMF's modest upgrade to global growth of 3.2% but caution about "rolling shocks" and downside-tilted risks, creating a stark contrast between near-term optimism and mounting structural concerns about asset valuations, systemic leverage, and technological disruption.

US-China Trade War Escalates with Rare Earth 'Bazooka' and Tariff Threats | Links: [4], [5], [6]

China has unleashed what analysts term its "rare earth bazooka", expanding export controls on critical materials including rare earth magnets and tightening licensing requirements that could cripple global technology and defence supply chains. Trump responded with characteristic force, threatening 100% tariffs on Chinese goods and a cooking oil embargo over Beijing's soybean purchasing boycott. Treasury nominee Scott Bessent escalated the rhetoric further, accusing China of trying "to pull everybody else down with them" as the conflict evolves. The escalation has triggered a scramble for alternative rare earth supplies, with China simultaneously retaliating against US firms including Qualcomm while banning Dutch semiconductor exports. What began as trade friction has transformed into a battle for control over materials essential to defence systems, renewable energy infrastructure, and consumer electronics.

Powell Signals Dovish Fed Pivot as Balance Sheet Reduction Nears End | Links: [7], [8], [9]

Fed Chair Powell provided significant policy guidance yesterday, suggesting quantitative tightening could conclude "in months ahead" while acknowledging troubling labour market dynamics despite describing the economy as on "firmer footing". Powell warned of a persistent "low-hiring, low-firing" trend that complicates the central bank's assessment, while noting that government shutdown data voids are hampering policy decisions. The dovish shift gained momentum as board member Collins stated it's "prudent to ease a bit more in 2025", marking a clear pivot from the Fed's restrictive stance. This accommodation comes as other major central banks reassess their tightening cycles, with the ECB's Lagarde unable to rule out further cuts and Bank of England members warning that elevated rates could push the UK into recession. The policy convergence highlights how’s global monetary authorities are prioritising growth support over inflation concerns.

Credit Suisse Bond Ruling Challenges European Banking Resolution Framework | Links: [10], [11]

A Swiss court has declared that the CHF 16.5 billion ($20 billion) AT1 bond write-off in Credit Suisse's emergency rescue was unlawful, fundamentally challenging the crisis management frameworks that European authorities have relied upon since the 2008 financial crisis. The unprecedented ruling questions the established resolution hierarchy where Additional Tier 1 bonds were completely wiped out while equity holders received value through UBS shares, creating regulatory uncertainty that extends far beyond Switzerland's borders. The decision could force comprehensive rewrites of bank resolution procedures across Europe and affect pricing throughout the €400 billion AT1 market, where investors had accepted higher yields based partly on clear regulatory frameworks for crisis scenarios. The ruling arrives at a particularly sensitive time as banking regulators across jurisdictions continue to grapple with lessons from the 2023 banking turmoil that claimed Credit Suisse, Silicon Valley Bank, and others.

Market Volatility Surge Reflects Shifting Risk Appetite | Links: [12], [13]

The VIX has climbed to five-month highs as escalating US-China trade tensions and Federal Reserve policy uncertainty drive volatility across global asset classes, with cryptocurrency markets shedding $150 billion in value while bond markets rallied on flight-to-safety flows. Yet Asian markets have shown remarkable resilience, rallying despite Wall Street's declines and suggesting a notable regional divergence in risk sentiment that could signal shifting capital flow patterns between major markets. This volatility surge demonstrates the confluence of multiple risk factors that have emerged simultaneously: geopolitical tensions over critical materials, monetary policy uncertainty from major central banks, and growing institutional warnings about elevated asset valuations. The disconnect between regional market performance suggests investors are becoming increasingly selective in their geographic and sector positioning rather than adopting broad risk-on or risk-off strategies, potentially creating new opportunities for those willing to navigate the complexity.

| S&P 500 | 6644.31+41.82▲ +0.63% |

| FTSE 100 | 9452.80+9.90▲ +0.10% |

| CAC 40 | 7919.62+56.71▲ +0.72% |

| DAX 40 | 24236.90+67.90▲ +0.28% |

| Dow Jones | 46270.50+398.60▲ +0.87% |

| Euro Stoxx 50 | 5552.05-0.44▼ -0.01% |

| Hang Seng | 25441.30-527.90▼ -2.03% |

| Nasdaq 100 | 24579.30+136.40▲ +0.56% |

| Nasdaq Comp | 22521.70+133.70▲ +0.60% |

| Nikkei 225 | 46847.30-599.40▼ -1.26% |

| S&P/ASX 200 | 8899.40+16.60▲ +0.19% |

| Shanghai Comp | 3865.23-45.55▼ -1.16% |

| S&P 500 E-mini | 6714.50+28.00▲ +0.42% |

| Nasdaq 100 | 24914.20+151.75▲ +0.61% |

| FTSE 100 | 9521.00+38.00▲ +0.40% |

| Euro Stoxx 50 | 5637.00+75.00▲ +1.35% |

| WTI Crude | 58.60-0.10▼ -0.17% |

| Gold | 4208.90+45.50▲ +1.09% |

| Copper | 5.04+0.01▲ +0.28% |

| US 10Y Treasury | 113.44+0.03▲ +0.03% |

| UK 10Y Gilt | 118.48+0.03▲ +0.03% |

| German 10Y Bund | 129.76+0.08▲ +0.06% |

| Italian 10Y BTP | 121.09+0.36▲ +0.30% |

| US Dollar Index | 98.65-0.17▼ -0.17% |

| VIX Volatility | 20.20-0.28▼ -1.39% |

| SONIA 3M | 96.17+0.04▲ +0.04% |

• UK BoE Ramsden Speech at 09:00 BST - Bank of England Deputy Governor's remarks could signal shifts in monetary policy stance amid evolving inflation dynamics.

• China New Yuan Loans at 10:00 BST - Forecast: ¥1,472.0B vs Previous: ¥590.0B - Sharp increase in credit extension could indicate aggressive stimulus measures supporting global commodity demand and risk sentiment.

• EU Industrial Production MoM at 10:00 BST - Forecast: -1.5% vs Previous: 0.3% - Expected contraction would confirm eurozone manufacturing weakness and weigh on EUR strength.

• US NY Empire State Manufacturing Index at 13:30 BST - Forecast: -7.0 vs Previous: -8.7 - Modest improvement in regional manufacturing sentiment could support USD and industrial sector equities.

• US Fed Bostic Speech at 17:10 BST - Atlanta Fed President's comments on interest rate outlook could move bond yields and currency markets ahead of next FOMC meeting.

• US Fed Waller Speech at 18:00 BST - Fed Governor's hawkish stance historically makes his remarks key for treasury markets and dollar direction.

• Japan Machinery Orders MoM at 00:50 BST (Thursday) - Forecast: 0.5% vs Previous: -4.6% - Recovery in capital expenditure plans would signal strengthening business confidence and support JPY.

No major earnings events scheduled for today.

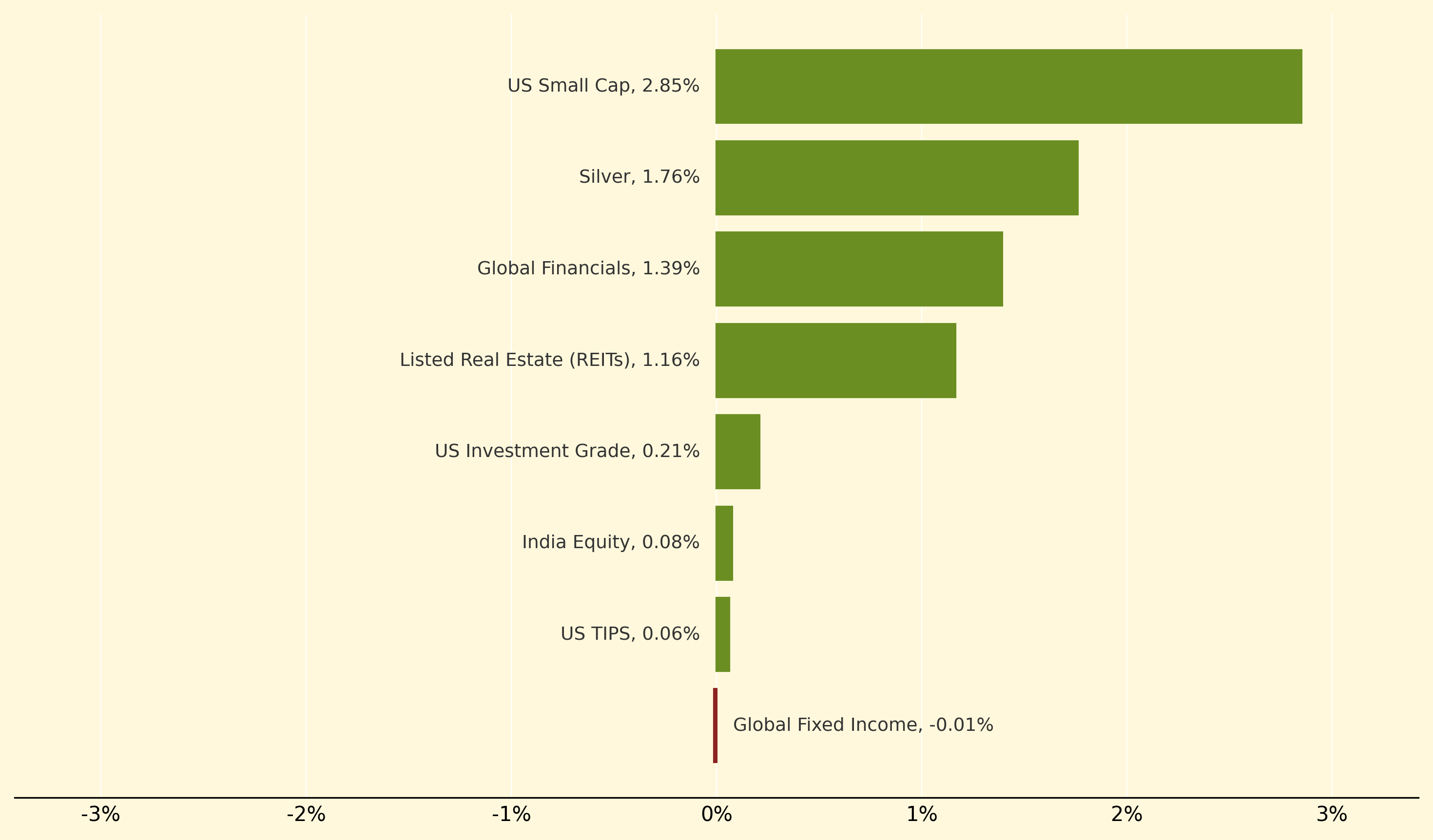

US Small Cap led yesterday's gains with a robust 2.85% surge, benefiting from Powell's dovish signals about potential Fed easing and balance sheet reduction ending soon. Silver also performed strongly at 1.76%, likely driven by safe-haven demand amid escalating US-China trade tensions and China's rare earth export restrictions, while Global Financials climbed 1.39% as major bank earnings exceeded expectations.

Conversely, fixed income strategies showed minimal movement, with Global Fixed Income essentially flat at -0.01% and US TIPS gaining just 0.06%, demonstrating muted bond market reactions despite flight-to-safety flows. India Equity managed only 0.08% gains despite the IMF raising India's growth forecast, suggesting regional performance diverged from broader emerging market optimism as investors remained cautious about trade war spillovers.

Quantitative tightening: The systematic reduction of a central bank's balance sheet by allowing bonds to mature without replacement, effectively removing money from the financial system and reversing the monetary stimulus provided through quantitative easing programmes during economic crises.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry