Trump's Tariff Ultimatum Triggers Global Market Rout | Links: [1], [2], [3]

Donald Trump's proposal for an additional 100% tariff on Chinese imports, combined with expanded export controls on critical software, has triggered the most significant market volatility since April. The S&P 500 declined 2.7% while the Nasdaq suffered its steepest drop in months, with tech megacaps shedding $770 billion in market value as investors rotated away from risk assets. Asian markets experienced pronounced weakness, with the Hang Seng falling 3.1% and Singapore's STI dropping 1.1%. China responded with retaliatory port fees on American vessels and rare earth export controls, extending the trade dispute beyond tariffs into strategic supply chains. The breadth of the market reaction—spanning equities, commodities, and cryptocurrencies which saw $6 billion in liquidations—demonstrates how US-China tensions have evolved into a systemic concern for global growth expectations.

Safe Haven Stampede Drives Gold to Record Highs Above $4,000 | Links: [4], [5], [6]

The developing trade tensions prompted a substantial movement to safety assets, with gold reaching record levels above $4,000 per ounce—a notable 54% advance year-to-date that indicates fundamental shifts in global risk appetite. Silver simultaneously reached decade-highs while Treasury bonds rallied as investors sought alternatives to the equity selloff, with Goldman Sachs raising its gold target to $4,900 in recognition of sustained institutional demand. The precious metals advance extends beyond trade war concerns to encompass broader questions about market valuations, as central bankers from the BoE, IMF, and ECB have been highlighting bubble risks across asset classes. This represents more than tactical positioning—the magnitude of gold's performance alongside falling risk assets indicates a structural reassessment of portfolio protection requirements in an increasingly fragmented global economy.

Political Chaos Engulfs Major Economies as Coalitions Crumble | Links: [7], [8], [9]

A wave of political instability is simultaneously affecting major economies, amplifying market uncertainty as governance structures face pressure from economic challenges. Japan's decades-old ruling coalition has collapsed, with potential PM candidate Sanae Takaichi advocating ultra-dovish monetary policy that's creating yen volatility and affecting global carry trade positioning. France confronts its own crisis as PM Lecornu attempts to navigate parliamentary arithmetic on critical budget legislation, threatening eurozone stability if the government falls. The US government shutdown entering its tenth day adds another layer of dysfunction, with substantial federal job cuts beginning and economic data releases disrupted just as the Fed requires clarity on policy direction. This simultaneous political paralysis across three major economies creates compounding risks for global policy coordination at precisely the moment markets need decisive leadership.

Bank Deregulation Unlocks $2.6 Trillion Wall Street Lending Capacity | Links: [10]

US bank deregulation is poised to unlock $2.6 trillion of Wall Street lending capacity, fundamentally reshaping the competitive landscape of global finance as American institutions gain significant advantages over international rivals. This regulatory shift occurs as US banks already benefit from higher interest rates and robust domestic demand, potentially creating a formidable combination for market share capture in global credit markets. The timing appears particularly strategic, coinciding with trade tensions and supply chain disruptions that are likely to increase demand for trade financing and corporate restructuring capital. European banks face mounting pressure as their American counterparts gain both regulatory flexibility and capital deployment advantages, while credit markets could see increased liquidity and potentially compressed spreads as competition intensifies for quality borrowers.

China's Export Resilience Strengthens Beijing's Hand in Trade War | Links: [11], [12], [13]

Despite mounting trade pressures, China's September export data surpassed expectations with 8.3% dollar-denominated growth, while imports increased 7.4%—the fastest pace since April 2024. This strong performance considerably enhances Beijing's negotiating position as trade tensions intensify, demonstrating economic resilience that likely emboldens Chinese policymakers to implement retaliatory measures including rare earth export controls and port fees on American vessels. The data indicates China's economy maintains momentum despite geopolitical headwinds, potentially explaining officials' confidence in adopting a firmer stance against US proposals. However, markets remain sceptical about sustainability, with Chinese equities continuing to decline even as Trump signalled potential openness to deal-making, reflecting deep uncertainty about whether economic fundamentals or geopolitical tensions will ultimately drive asset prices.

| Dow Jones Industrial Average | 45479.60-915.30▼ -1.97% |

| S&P 500 | 6552.51-187.98▼ -2.79% |

| Hang Seng Index | 26290.30-233.60▼ -0.88% |

| FTSE 100 | 9427.50-81.90▼ -0.86% |

| CAC 40 | 7918.00-131.57▼ -1.63% |

| DAX 40 | 24241.50-422.70▼ -1.71% |

| Euro Stoxx 50 | 5531.32-97.51▼ -1.73% |

| Nasdaq Composite | 22204.40-839.10▼ -3.64% |

| Nasdaq-100 | 24221.70-895.10▼ -3.56% |

| Nikkei 225 | 48088.80-421.90▼ -0.87% |

| S&P/ASX 200 | 8958.30-11.50▼ -0.13% |

| Shanghai Composite | 3897.03-18.45▼ -0.47% |

| S&P 500 E-mini | 6679.50+84.25▲ +1.28% |

| Nasdaq-100 | 24816.00+419.00▲ +1.72% |

| FTSE 100 Index | 9463.00-0.50▼ -0.01% |

| EURO STOXX 50 | 5566.00+22.00▲ +0.40% |

| WTI Crude Oil | 59.79+0.89▲ +1.51% |

| Gold (COMEX) | 4085.00+84.60▲ +2.11% |

| Copper (COMEX) | 5.00+0.11▲ +2.27% |

| US 10-Year Treasury | 113.00-0.14▼ -0.12% |

| UK Long Gilt (10Y) | 118.18-0.06▼ -0.05% |

| German Bund (10Y) | 129.18-0.13▼ -0.10% |

| Italian BTP (10Y) | 120.61+0.53▲ +0.44% |

| US Dollar Index | 98.69-0.05▼ -0.05% |

| VIX Volatility | 19.75-1.26▼ -5.99% |

| SONIA 3M Interest Rate | 96.12+0.01▲ +0.01% |

• Australian RBA Meeting Minutes on Tuesday at 01:30 BST - Previous: 4.0 - Key insights into the RBA's latest policy stance and future rate trajectory affecting AUD and regional markets.

• UK Unemployment Rate on Tuesday at 07:00 BST - Forecast: 4.7% vs Previous: 4.7% - Critical labour market indicator influencing BoE policy expectations and GBP direction.

• German ZEW Economic Sentiment Index on Tuesday at 10:00 BST - Forecast: 39.5 vs Previous: 37.3 - Leading indicator of German economic outlook impacting EUR and European equity markets.

• US Fed Chair Powell Speech on Tuesday at 17:20 BST - Major policy communication potentially signalling Fed's future rate path and market direction.

• Chinese Inflation Rate YoY on Wednesday at 02:30 BST - Forecast: -0.1% vs Previous: -0.4% - Deflationary pressures could prompt further stimulus measures affecting global commodities and risk sentiment.

• UK GDP MoM on Thursday at 07:00 BST - Forecast: 0.2% vs Previous: 0.0% - Growth momentum crucial for BoE policy decisions and GBP performance.

• US PPI MoM on Thursday at 13:30 BST - Forecast: 0.3% vs Previous: -0.1% - Producer price inflation feeding into Fed policy considerations and bond market movements.

• US Retail Sales MoM on Thursday at 13:30 BST - Forecast: 0.4% vs Previous: 0.6% - Consumer spending strength indicator affecting Fed policy outlook and equity markets.

• American Express (AXP) on Friday at 12:00 BST Pre-Market - $220.1B - Major Dow component and credit card bellwether, earnings will signal consumer spending trends and credit quality in the current economic environment.

• Reliance Industries (RELIANCE) on Friday at 13:00 BST Pre-Market - $210.6B - India's largest conglomerate and key emerging market indicator, results will reflect energy sector performance and Indian economic health.

• HDFC Bank (HDFCBANK) on Saturday at 13:00 BST Pre-Market - $169.7B - India's largest private bank and major emerging market financial stock, critical for assessing Indian banking sector strength and loan growth.

• Zijin Mining (601899) on Saturday at 13:00 BST Pre-Market - $114.7B - Major Chinese gold and copper producer, earnings will indicate commodity demand trends and Chinese industrial activity.

• ICICI Bank (ICICIBANK) on Saturday at 13:00 BST Pre-Market - $111.1B - India's second-largest private bank, results will complement HDFC's outlook on Indian financial sector and economic growth prospects.

• Volvo (VOLV_A) on Friday at 06:20 BST Pre-Market - $56.9B - European industrial bellwether and truck manufacturer, earnings will signal commercial vehicle demand and European industrial activity.

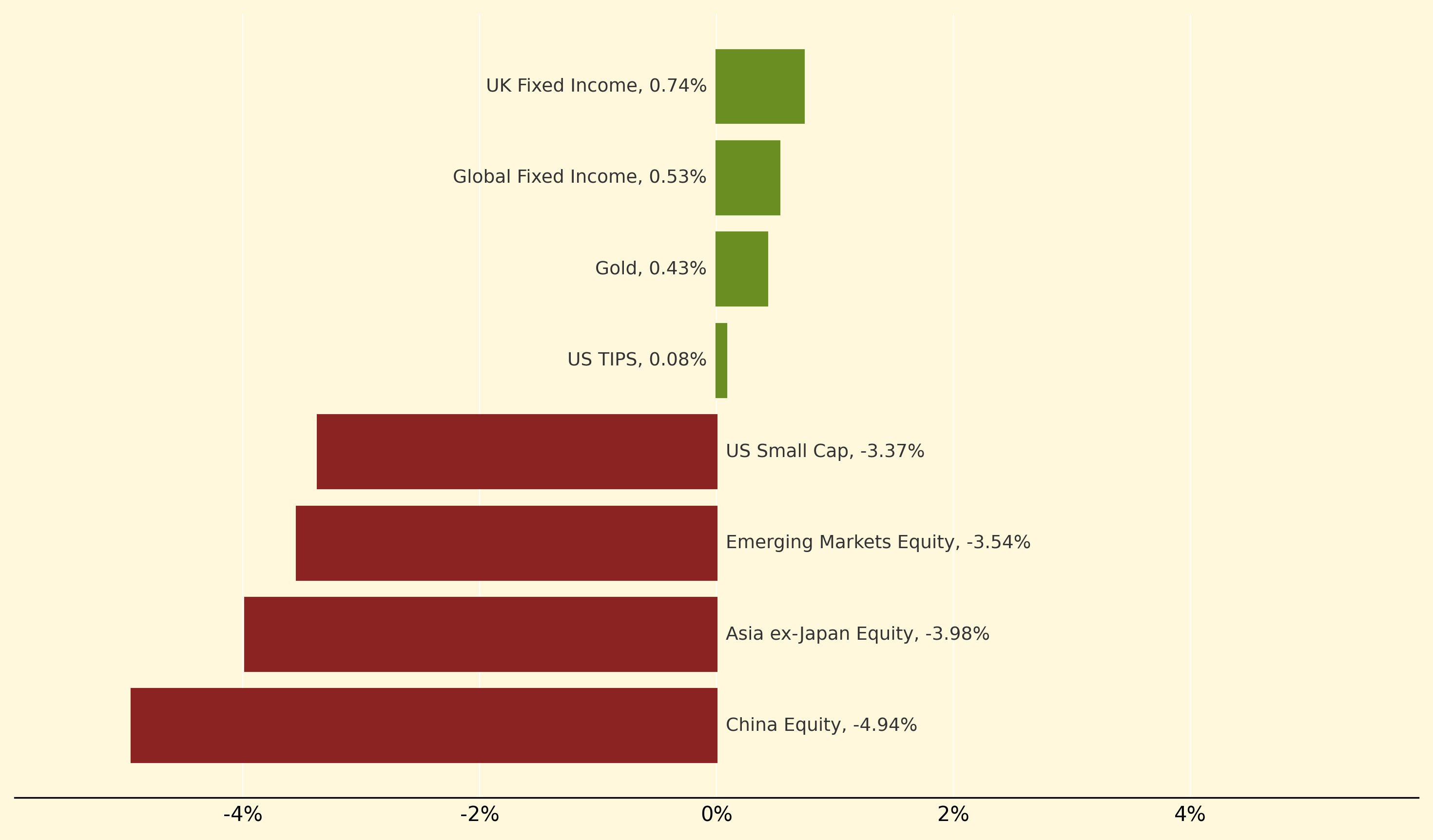

UK Fixed Income led defensive assets higher, climbing 0.74% as Trump's tariff proposal triggered a massive rotation to safety across global markets. Global Fixed Income also advanced 0.53%, while Gold gained 0.43% amid the developing trade tensions that pushed precious metals to record highs above $4,000 per ounce.

China Equity suffered the steepest decline, falling 4.94% as Beijing faced the brunt of Trump's proposed 100% tariff increase and expanded export controls. Asia ex-Japan Equity dropped 3.98% and Emerging Markets Equity declined 3.54%, reflecting broad-based selling across risk assets as investors reduced developing market exposure amid the renewed US-China trade conflict.

Export controls: Government restrictions on selling specific goods, technologies, or services to foreign entities, typically targeting strategic sectors like semiconductors or software to limit adversaries' access to critical capabilities that could enhance military or economic competitiveness.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry