Gold Reaches $3,900 as Multiple Crises Drive Safe-Haven Demand | Links: [1], [2], [3]

Gold broke through $3,900 per ounce to fresh all-time highs yesterday, bringing the psychological $4,000 level tantalizingly close as investors fled mounting global uncertainty. The precious metal's extraordinary 48% year-to-date gain reflects unprecedented safe-haven demand driven by America's government shutdown, France's political collapse, and broader concerns about dollar hegemony and fiscal sustainability across major economies. Citadel's Ken Griffin captured the mood, calling the flight to gold "really concerning" and highlighting systemic fears about currency debasement that are reshaping portfolio allocations. The rally represents one of the most significant repositioning moves across asset classes this year, with massive implications for traditional 60/40 strategies as investors scramble to hedge against what many view as coordinated policy failures across developed nations.

France Descends Into Unprecedented Political Crisis as Government Collapses | Links: [4], [5], [6]

France entered its deepest political crisis in modern history as Prime Minister Lecornu resigned just 12 hours after his appointment, creating unprecedented instability in the eurozone's second-largest economy. French markets tumbled with equities posting their steepest fall in over a month, whilst government bond spreads widened significantly versus German bunds as credit rating agencies issued fresh warnings about the country's deteriorating fiscal position. With debt-to-GDP approaching 115% and budget deficits running at double EU limits, analysts now consider French bonds riskier than Italy's, with some labelling them "uninvestable." President Macron faces stark choices: appoint another prime minister who can survive parliament, call snap elections that could strengthen extremist parties, or potentially resign himself. The political paralysis comes at a critical juncture for European unity, with contagion risks spreading across peripheral eurozone debt markets as investors reassess sovereign risk assumptions that held for over a decade.

Fed Officials Signal Hawkish Stance Despite Market Rate Cut Expectations | Links: [7], [8]

Fed regional president Schmid declared interest rates "appropriately calibrated" and pushed back against further cuts, citing persistent services inflation running at 3.5% - well above the central bank's comfort zone. This hawkish stance creates a striking contrast with market expectations of continued easing and President Trump's vocal demands for steep rate reductions despite simultaneously claiming a "booming" economy. The divergence highlights growing tension between political pressure for accommodation and Fed independence, with policymakers increasingly concerned that services inflation - which covers everything from healthcare to housing - remains stubbornly elevated despite headline progress. The disconnect between Fed rhetoric and market pricing indicates potential volatility ahead as investors grapple with the possibility that monetary policy may remain more restrictive for longer than anticipated, particularly if political pressure continues to build.

AI Sector Ignites 'Everything Rally' as AMD-OpenAI Partnership Shakes Markets | Links: [9], [10], [11]

US indices reached all-time closing highs as AI dealmaking reached fever pitch, with AMD surging 24% on news of a major multi-gigawatt GPU deployment partnership with OpenAI that includes an option for the AI company to take a 10% stake in the chipmaker. The deal directly challenges Nvidia's dominance in AI infrastructure and reflects OpenAI's expanding influence - analysts noted the company now possesses the power to move seemingly unrelated stocks through partnership announcements alone. This concentration of capital flows into the "AI industry's happy few" prompted veteran investor Paul Tudor Jones to warn that ingredients are in place for a massive rally followed by a potential "blow off" top reminiscent of the dot-com era. The divergence between AI euphoria and broader economic uncertainty creates an unusual market dynamic where tech speculation thrives amid political chaos, indicating either remarkable resilience or dangerous complacency among equity investors.

Emerging Markets Experience Biggest Rally in 15 Years as Dollar Weakens | Links: [12], [13]

Emerging market equities recorded their strongest rally in 15 years as dollar weakness and yield-seeking behaviour drive capital away from increasingly volatile developed market government bonds toward more stable emerging market assets. The broad-based rally reflects genuine structural improvements, with the IMF noting that better policies and deeper financial markets have helped emerging economies weather recent shocks whilst adding approximately 0.5 percentage points to their growth potential. This transformation comes as developed market politics grow more unpredictable - from France's constitutional crisis to America's shutdown dysfunction - making emerging markets appear relatively stable and attractively valued by comparison. The reversal of traditional risk hierarchies demonstrates a fundamental shift in global capital allocation, with investors increasingly viewing emerging market debt and equities as diversification tools against developed market political risk rather than sources of volatility themselves.

| Dow Jones Industrial Average | --▼ -0.17% |

| S&P 500 | --▲ +0.10% |

| Hang Seng Index | --▼ -0.17% |

| FTSE 100 | --▼ -0.13% |

| CAC 40 | --▼ -0.79% |

| DAX 40 | --▲ +0.08% |

| Euro Stoxx 50 | --▼ -0.47% |

| Nasdaq Composite | --▲ +0.21% |

| Nasdaq-100 | --▼ -0.03% |

| Nikkei 225 | --▲ +2.81% |

| S&P/ASX 200 | --▼ -0.07% |

| S&P 500 E-mini | 6784.00-4.75▼ -0.07% |

| Nasdaq-100 | 25178.20-6.50▼ -0.03% |

| FTSE 100 Index | 9519.00-7.00▼ -0.07% |

| EURO STOXX 50 | 5642.00-3.00▼ -0.05% |

| WTI Crude Oil | 61.76+0.07▲ +0.11% |

| Gold (COMEX) | 3985.10+8.80▲ +0.22% |

| Copper (COMEX) | 5.08+0.05▲ +0.89% |

| US 10-Year Treasury | 112.45+0.06▲ +0.06% |

| UK Long Gilt (10Y) | 117.86+0.00▲ +0.00% |

| German Bund (10Y) | 128.52-0.04▼ -0.03% |

| Italian BTP (10Y) | 119.79-0.18▼ -0.15% |

| US Dollar Index | 97.94+0.16▲ +0.16% |

| VIX Volatility | 17.55-0.05▼ -0.30% |

| SONIA 3M Interest Rate | 96.12+0.00▼ -0.01% |

• German Factory Orders MoM at 07:00 BST - Forecast: 1.2% vs Previous: -2.9% - A strong rebound could signal recovery in Europe's largest economy and support the euro.

• US Balance of Trade at 13:30 BST - Forecast: -$61.0B vs Previous: -$78.3B - Narrowing deficit would indicate improving competitiveness and could strengthen the dollar amid trade policy focus.

• Canadian Ivey PMI s.a at 15:00 BST - Forecast: 51.2 vs Previous: 50.1 - Expansion above 50 signals strengthening business conditions and may influence Bank of Canada policy expectations.

• EU ECB President Lagarde Speech at 17:10 BST - Key insights on monetary policy direction and inflation outlook could drive euro volatility and bond market movements.

• Japanese Current Account at 00:50 BST (Wednesday) - Forecast: ¥3540.0B vs Previous: ¥2684.0B - Larger surplus reflects strong export performance and supports yen strength amid global trade dynamics.

No major earnings events scheduled for today.

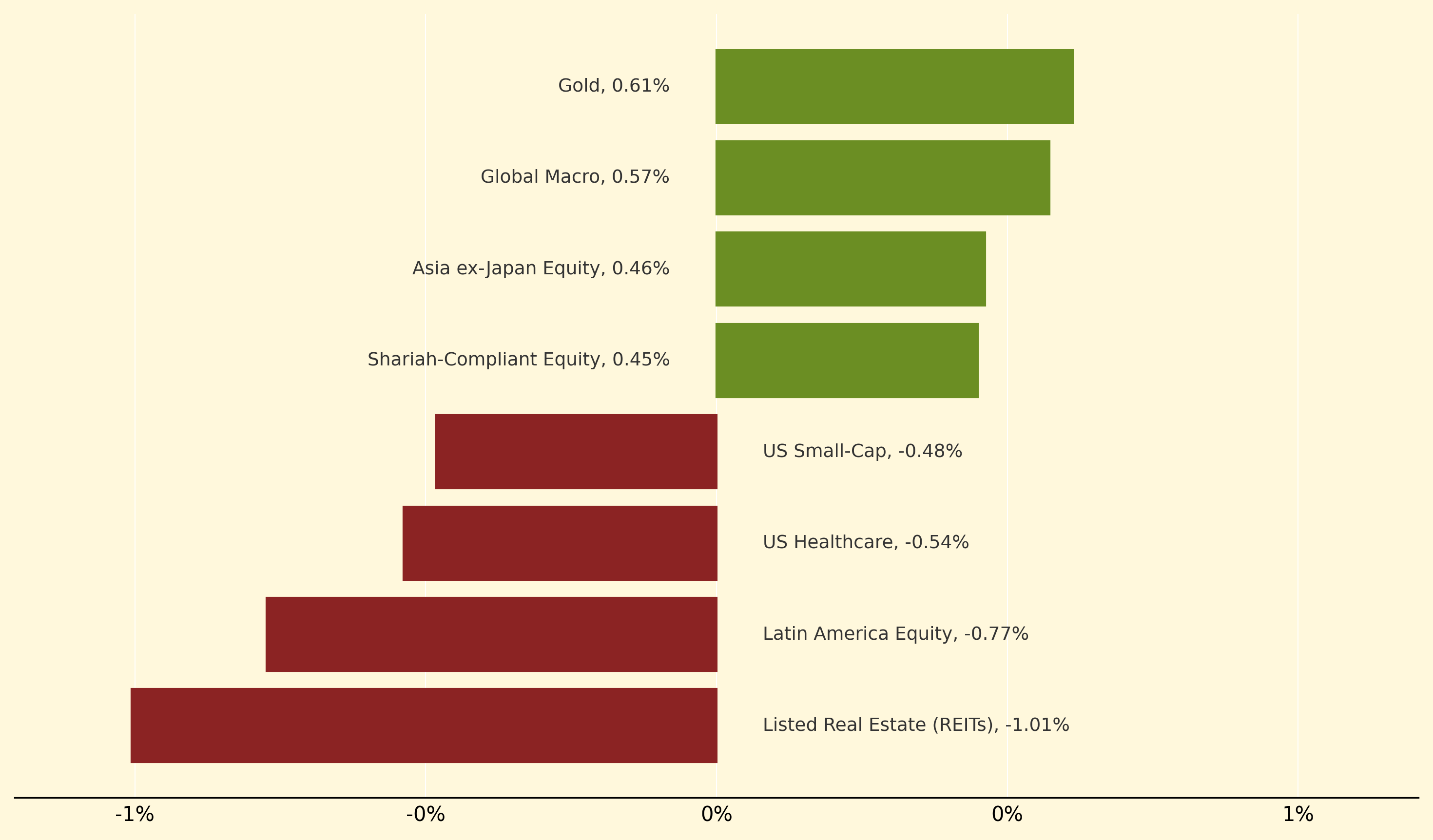

Gold led gains with a 0.61% advance as safe-haven demand intensified amid France's unprecedented political crisis and the ongoing US government shutdown, pushing the precious metal past $3,900 toward the psychological $4,000 level. Global Macro strategies also performed well, climbing 0.57%, whilst Asian equity exposure benefited from regional outperformance, with Asia ex-Japan and China Equity strategies gaining 0.46% and 0.41% respectively.

Conversely, Listed Real Estate (REITs) suffered the steepest decline at -1.01% as heightened uncertainty and political instability weighed on rate-sensitive assets. Latin America Equity also underperformed significantly, dropping -0.77%, whilst US-focused dividend and healthcare strategies lagged with US High Dividend Yield falling -0.43% and US Healthcare declining -0.54% amid broader concerns about domestic political stability.

Blow off top: A sharp, unsustainable market rally driven by extreme speculation and euphoria that precedes a dramatic crash, characterised by parabolic price acceleration and widespread investor complacency before sentiment suddenly reverses.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry