Japanese Stocks Hit Records as 'Takaichi Trade' Ignites Global Policy Divergence | Links: [1], [2], [3]

Sanae Takaichi's victory as Japan's likely first female Prime Minister has triggered a seismic repricing across global markets, with the Nikkei surging 4% to record highs above 47,000 whilst the yen crashed past 150 against the dollar. Her 'Abenomics revival' agenda—opposing Bank of Japan rate hikes and championing aggressive fiscal expansion—has effectively derailed October's anticipated BOJ tightening and reignited what traders call the 'Takaichi trade.' The policy pivot extends beyond monetary dovishness to increased defence spending and nuclear energy prioritisation, driving dramatic sector rotation into Japanese defence and technology stocks. Goldman Sachs warns this Japanese bond volatility could spill into US Treasuries, given Japan's substantial foreign debt holdings and the interconnected nature of global fixed income markets. For managers, this represents a fundamental repricing of one of the world's largest equity markets and a critical source of global liquidity through carry trades.

Alternative Assets Surge as 'Debasement Trade' Accelerates Amid Policy Chaos | Links: [4], [5], [6]

Gold has breached $3,900 whilst approaching $4,000 as Bitcoin reaches record highs above $125,000, driven by what JPMorgan analysts term the 'debasement trade'—a coordinated flight from traditional currencies amid cascading policy uncertainty. The surge reflects converging chaos: Japanese monetary policy divergence, the ongoing US government shutdown disrupting critical economic data including employment reports, and mounting concerns about fiscal sustainability across major economies. The 50% rally in gold this year represents what analysts call 'gold-plated FOMO' among institutional investors, whilst Bitcoin's records signal broader digital asset acceptance as an inflation hedge. This movement beyond traditional safe havens reflects deeper anxieties about monetary policy effectiveness and currency debasement, with implications extending into fundamental portfolio construction and risk management strategies.

Fed Policy Divergence Emerges as Data Shutdown Clouds Economic Picture | Links: [7], [8], [9]

The US government shutdown has suspended critical economic data flows precisely when Fed policymakers need clarity for their 'meeting-by-meeting' approach, with the crucial October jobs report cancelled and officials operating in an information vacuum ahead of the October 28-29 FOMC meeting. This compounds existing Fed tensions, with Governor Miran advocating aggressive 50bp cuts whilst President Goolsbee warns against 'front-loading too many rate cuts' amid persistent services inflation. BofA has accelerated its Fed cut forecast to October from December, but the data blackout increases policy uncertainty for markets heavily dependent on US labour data for guidance. Bloomberg reports global central banks are set to diverge sharply—the Fed driving cuts whilst European central banks shift toward policy pauses, creating complex cross-currency dynamics and interest rate differential trades that require careful navigation in an environment where traditional data anchors have disappeared.

AI Bubble Warnings Intensify from Major Institutional Voices | Links: [10], [11]

Singapore's sovereign wealth fund GIC has joined an increasingly vocal chorus of sophisticated institutional investors warning about AI bubble risks, with analysis suggesting the 'AI capex endgame is approaching' as excess capacity concerns mount. GIC's chief investment officer adds credibility to growing scepticism about trillion-dollar AI valuations amid signs that capital expenditure may be dramatically outpacing realistic demand projections. The timing proves particularly significant as companies continue massive AI infrastructure investments whilst evidence of sustainable returns remains elusive. For portfolio managers, this represents a potential inflection point where institutional sentiment could drive meaningful sector rotation away from high-multiple AI plays toward more defensive positioning. These warnings carry weight precisely because they originate from some of the world's most sophisticated institutional investors, rather than retail sentiment or media speculation.

Energy Markets Signal Structural Shifts as OPEC+ Caution Meets Supply Constraints | Links: [12], [13], [14]

Global energy markets display critical structural tensions as OPEC+ opts for modest 137,000 bpd output increases amid mounting supply glut fears, whilst spare capacity erodes to historically dangerous levels around 2% of global demand. Fatal accidents at Freeport's Grasberg mine—one of the world's largest copper producers—have extended copper's gains, highlighting how supply disruptions rapidly impact industrial metals amid Fed easing expectations. This combination of constrained oil shock absorbers and base metals supply risks creates volatile conditions for commodity-exposed portfolios, whilst the broader debasement dynamic extends into commodities as investors seek inflation hedges beyond traditional assets. Despite current oil weakness, underlying supply vulnerabilities could trigger rapid price reversals, whilst industrial metals benefit from both supply constraints and monetary policy tailwinds—a dynamic that demands more active commodity hedging strategies.

| Dow Jones Industrial Average | --▲ +0.37% |

| S&P 500 | --▼ -0.09% |

| Hang Seng Index | --▼ -0.30% |

| FTSE 100 | --▲ +0.67% |

| CAC 40 | --▼ -0.14% |

| DAX 40 | --▼ -0.54% |

| Euro Stoxx 50 | --▼ -0.11% |

| Nasdaq Composite | --▼ -0.46% |

| Nasdaq-100 | --▼ -0.59% |

| Nikkei 225 | --▲ +1.61% |

| S&P/ASX 200 | --▲ +0.46% |

| S&P 500 E-mini | 6782.75+18.75▲ +0.28% |

| Nasdaq-100 | 25090.00+98.00▲ +0.39% |

| FTSE 100 Index | 9529.00-3.50▼ -0.04% |

| EURO STOXX 50 | 5669.00+3.00▲ +0.05% |

| WTI Crude Oil | 61.66+0.78▲ +1.28% |

| Gold (COMEX) | 3960.60+51.70▲ +1.32% |

| Copper (COMEX) | 5.09-0.02▼ -0.44% |

| US 10-Year Treasury | 112.47-0.20▼ -0.18% |

| UK Long Gilt (10Y) | 117.75-0.09▼ -0.08% |

| German Bund (10Y) | 128.42-0.25▼ -0.19% |

| Italian BTP (10Y) | 119.97+0.07▲ +0.06% |

| US Dollar Index | 97.80+0.39▲ +0.40% |

| VIX Volatility | 17.65-0.08▼ -0.44% |

| SONIA 3M Interest Rate | 96.12+0.00▲ +0.01% |

• AU Westpac Consumer Confidence Change on Tuesday at 01:30 BST - Previous: -3.1 - Key gauge of Australian consumer sentiment that influences RBA policy decisions and AUD volatility.

• DE Factory Orders MoM on Tuesday at 07:00 BST - Forecast: 1.2% vs Previous: -2.9% - Critical indicator of German manufacturing demand and eurozone industrial recovery prospects.

• US Balance of Trade on Tuesday at 13:30 BST - Forecast: -$61.0B vs Previous: -$78.3B - Major dollar driver reflecting trade dynamics and economic competitiveness.

• CA Ivey PMI s.a on Tuesday at 15:00 BST - Forecast: 51.2 vs Previous: 50.1 - Key Canadian business activity gauge influencing BoC policy expectations and CAD direction.

• US FOMC Minutes on Wednesday at 20:00 BST - Detailed insights into Fed officials' September rate decision rationale and future policy path guidance.

• DE Balance of Trade on Thursday at 07:00 BST - Forecast: €15.1B vs Previous: €14.7B - Germany's export strength indicator crucial for eurozone economic health and EUR sentiment.

• US Initial Jobless Claims on Thursday at 13:30 BST - Forecast: 223K vs Previous: 218K - Weekly employment health check affecting Fed policy expectations and market risk appetite.

• CA Unemployment Rate on Friday at 13:30 BST - Forecast: 7.1% vs Previous: 7.1% - Critical for BoC rate decisions and CAD positioning ahead of policy meetings.

• US Michigan Consumer Sentiment Prel on Friday at 15:00 BST - Forecast: 55.0 vs Previous: 55.1 - Consumer confidence gauge impacting retail sector outlook and Fed policy considerations.

• PepsiCo (PEP) on Thursday at 11:00 BST Pre-Market - $194.4B - Major S&P 500 consumer staples bellwether will provide insights into inflation pressures and consumer spending trends across global markets.

• Progressive Corporation (PGR) on Thursday at 13:00 BST Pre-Market - $144.0B - Leading US auto insurer's results will signal consumer financial health and insurance sector pricing power amid economic uncertainty.

• Tata Consultancy Services (TCS) on Thursday at 13:00 BST Pre-Market - $118.3B - India's largest IT services company will indicate global technology spending trends and outsourcing demand from Western corporations.

• Fast Retailing (9983) on Thursday at 13:00 BST Pre-Market - $96.8B - Uniqlo parent company's performance will reflect Asian consumer sentiment and global retail sector health.

• HCL Technologies (HCLTECH) on Thursday at 13:00 BST Pre-Market - $42.6B - Major Indian IT services provider will complement TCS results in gauging enterprise technology investment trends.

• Delta Air Lines (DAL) on Thursday at 11:30 BST Pre-Market - $37.4B - Leading US carrier's earnings will provide crucial insights into travel demand recovery and fuel cost pressures affecting the aviation sector.

• Avenue Supermarts (DMART) on Saturday at 13:00 BST Pre-Market - $32.4B - India's dominant retail chain will indicate emerging market consumer spending and retail sector expansion trends.

• Zegona Communications (ZEG) on Monday at 13:00 BST Pre-Market - $13.6B - UK-focused telecom investment company will provide insights into European telecommunications sector consolidation and infrastructure investment.

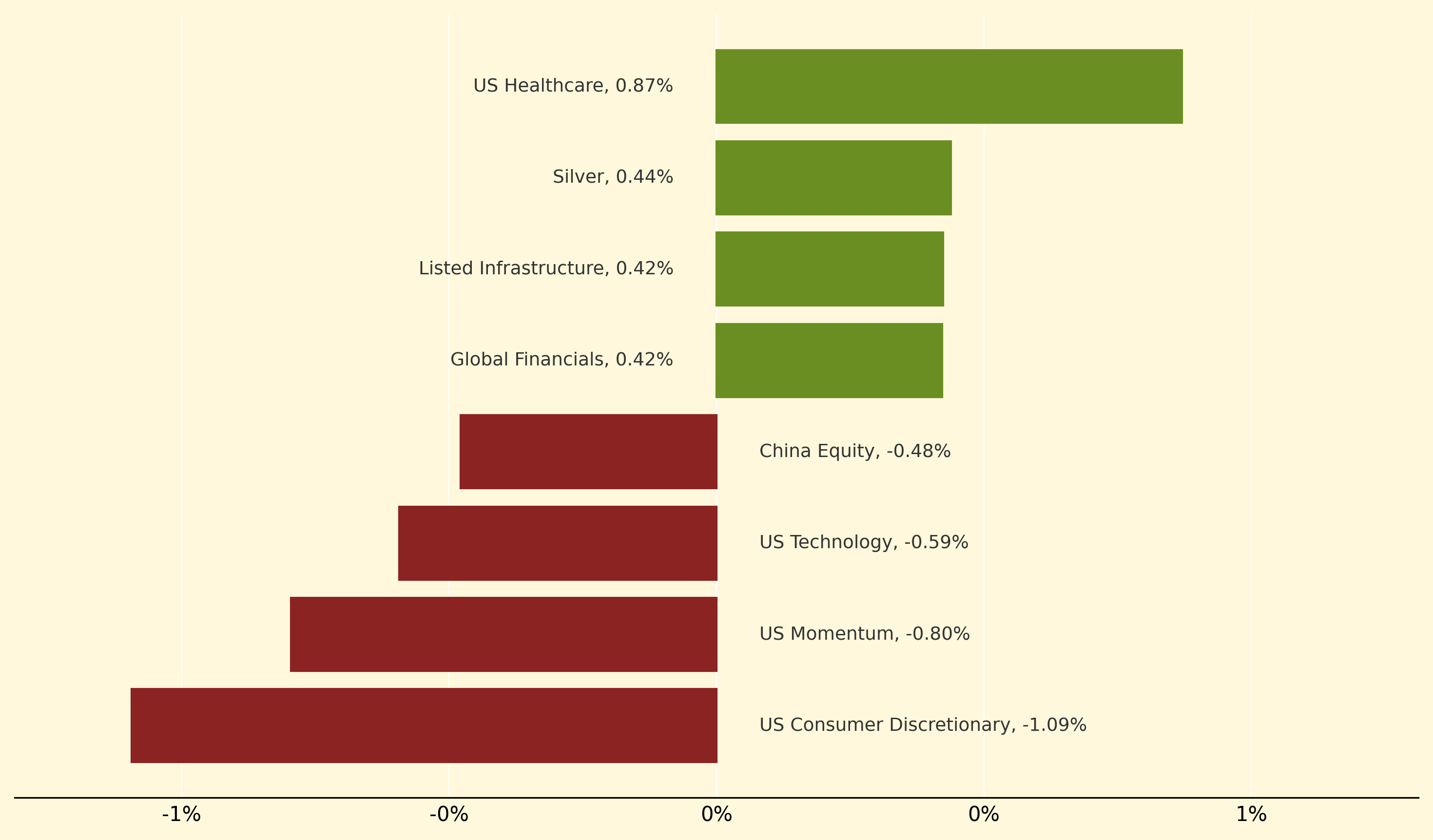

US Healthcare led gains, climbing 0.87% as defensive positioning benefited from broader market uncertainty amid the ongoing government shutdown and Fed policy divergence. Silver advanced 0.44% alongside the broader debasement dynamic driving alternative assets, whilst Listed Infrastructure and Global Financials both gained 0.42% as investors sought yield-generating assets amid monetary policy shifts.

Conversely, US Consumer Discretionary underperformed significantly, dropping 1.09% as spending concerns mounted amid political uncertainty and data blackouts. US Momentum also lagged, falling 0.8%, whilst US Technology declined 0.59% despite continued AI investment flows, reflecting growing institutional bubble warnings from sophisticated investors like GIC's sovereign wealth fund.

Debasement trade: A coordinated investment strategy involving flight from traditional fiat currencies into alternative assets like gold, Bitcoin, and commodities, driven by fears that aggressive monetary policies and fiscal spending will erode currency purchasing power and spark inflation.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry