Trump's Sectoral Tariff Blitz Triggers Global Market Rout | Links: [1], [2], [3]

President Trump escalated his trade war with surgical precision yesterday, announcing 100% tariffs on branded pharmaceuticals and 25% levies on heavy trucks and furniture imports, effective October 1st. Unlike previous broad-based measures, this calculated sector-specific assault targets critical supply chains with limited substitutability—particularly pharmaceuticals, where the tariff represents the most aggressive trade action yet on a sector worth billions globally. Asian markets absorbed the immediate shock, with Indian pharma and IT stocks leading a regional selloff as investors grappled with potential disruption to the $10.5 billion in pharmaceutical exports to the US. The pharmaceutical focus carries particular weight given the sector's high intellectual property content and global manufacturing footprint, forcing immediate supply chain reorganisation decisions across multinational corporations.

Global Debt Hits Record $338 Trillion Amid Systemic Risk Warnings | Links: [4], [5]

The Institute of International Finance reported global debt reached a record $337.7 trillion, with a staggering $21 trillion increase in just the first half—matching pandemic-era surge rates and signalling renewed fiscal and monetary stimulus dependency. The acceleration carries particular menace for emerging markets facing $3.2 trillion in bond redemptions, while developed markets show concerning debt-to-GDP deterioration. The IIF explicitly warned of potential "bond vigilante" scenarios where investors demand higher yields to compensate for fiscal risks, a prospect that gains credibility as corporate credit markets show early stress indicators despite continued institutional appetite. This debt mountain constrains central bank flexibility precisely when trade tensions and geopolitical risks demand policy responsiveness, creating a dangerous feedback loop between fiscal sustainability and monetary policy effectiveness.

European Banks Launch Euro Stablecoin to Counter US Dominance | Links: [6]

Nine major European banks moved to challenge US dominance in digital payments infrastructure, forming a company to launch a euro-denominated stablecoin targeting the $300 billion global stablecoin market. The initiative represents a direct challenge to dollar hegemony in digital finance, where US-controlled stablecoins like USDC and Tether currently dominate cross-border payment flows. Traditional banking giants across Europe are positioning themselves before regulatory frameworks solidify, recognising that stablecoin infrastructure could reshape international payment systems within the decade. The timing reflects growing European concern about financial sovereignty as digital currencies mature from experimental tools to critical payment rails, potentially reducing European dependence on US-controlled financial infrastructure at a moment when geopolitical tensions make such independence increasingly valuable.

Fed Policy Uncertainty Deepens as Strong Data Challenges Dovish Pivot | Links: [7], [8], [9]

Robust US economic data yesterday challenged expectations for aggressive Federal Reserve easing, with Q2 GDP revised sharply higher to 3.8% growth while jobless claims plummeted to 218,000—well below the 235,000 estimate. Core capital goods orders unexpectedly rose 2.9% in August, signalling business investment resilience that prompted market repricing from 125 to 100 basis points of cuts through year-end. The data confluence arrives amid unprecedented political pressures on Fed independence, highlighted by Governor Cook's warning of "market chaos" if Trump fires her, while bank reserves falling below $3 trillion for seven consecutive weeks signals liquidity constraints that could limit policy flexibility regardless of economic conditions. This combination of vigorous real activity, political interference risks, and technical liquidity drainage creates a particularly complex backdrop for monetary policy as the Fed navigates between economic strength and institutional survival.

Oil Surges to Biggest Weekly Gain in Three Months on Russia Supply Cuts | Links: [10], [11], [12]

Oil prices notched their strongest weekly performance since April as Russia imposed emergency diesel export restrictions following intensified Ukrainian strikes on refinery infrastructure. Russia's partial export bans through year-end respond to systematic Ukrainian targeting of energy facilities, creating actual supply disruptions rather than mere geopolitical premiums—diesel shortages are materialising in European markets as the country's 86 million tons of annual production capacity faces systematic attack. Ukrainian drone strikes near nuclear facilities, including incidents at the South Ukraine nuclear plant, compound risks beyond immediate energy impacts while the US intensifies pressure on Russian energy buyers. What distinguishes this episode from previous oil rallies is the direct supply impact hitting European diesel markets, raising systematic risks that could feed through to global inflation expectations and constrain central bank easing cycles precisely when other pressures already limit monetary policy flexibility.

| Dow Jones Industrial Average | --▼ -0.33% |

| S&P 500 | --▼ -0.05% |

| Hang Seng Index | --▼ -0.19% |

| FTSE 100 | --▼ -0.39% |

| CAC 40 | --▼ -0.03% |

| DAX 40 | --▼ -0.36% |

| Euro Stoxx 50 | --▼ -0.34% |

| Nasdaq Composite | --▲ +0.30% |

| Nasdaq-100 | --▲ +0.31% |

| Nikkei 225 | --▲ +0.34% |

| S&P/ASX 200 | --▲ +0.10% |

| Shanghai Composite | --▲ +0.02% |

| S&P 500 E-mini | 6656.25-3.50▼ -0.05% |

| Nasdaq-100 | 24595.50-33.75▼ -0.14% |

| FTSE 100 Index | 9277.00+18.50▲ +0.20% |

| EURO STOXX 50 | 5463.00+17.00▲ +0.31% |

| WTI Crude Oil | 65.22+0.24▲ +0.37% |

| Gold (COMEX) | 3774.40+3.30▲ +0.09% |

| Copper (COMEX) | 4.79+0.03▲ +0.71% |

| US 10-Year Treasury | 112.28-0.05▼ -0.04% |

| UK Long Gilt (10Y) | 117.51-0.02▼ -0.02% |

| German Bund (10Y) | 127.95-0.05▼ -0.04% |

| Italian BTP (10Y) | 119.22-0.30▼ -0.25% |

| US Dollar Index | 98.03-0.11▼ -0.11% |

| VIX Volatility | 18.35+0.02▲ +0.09% |

| SONIA 3M Interest Rate | 96.12-0.02▼ -0.02% |

• US Personal Spending MoM at 13:30 BST - Forecast: 0.5% vs Previous: 0.5% - Key gauge of consumer demand that drives two-thirds of US economic activity and influences Fed policy decisions.

• US Core PCE Price Index MoM at 13:30 BST - Forecast: 0.2% vs Previous: 0.3% - The Fed's preferred inflation measure that directly impacts interest rate expectations and dollar strength.

• US Personal Income MoM at 13:30 BST - Forecast: 0.3% vs Previous: 0.4% - Critical for assessing consumer spending power and economic momentum heading into year-end.

• EU ECB President Lagarde Speech at 10:30 BST - Could signal ECB's policy stance amid eurozone economic weakness and provide euro direction.

• CA GDP MoM at 13:30 BST - Forecast: 0.1% vs Previous: -0.1% - Potential return to growth for Canada's economy after contraction could impact BoC policy outlook.

• US Michigan Consumer Sentiment Final at 15:00 BST - Forecast: 55.9 vs Previous: 58.2 - Final reading on US consumer confidence as markets assess holiday spending potential.

• Zegona Communications Plc (ZEG) at 13:00 BST [Pre-Market] - Est: N/A vs Prev: N/A - European telecom consolidation play could signal broader M&A activity in the sector.

• New World Development Co. Ltd. (17) at 13:00 BST [Pre-Market] - Est: $0.11 vs Prev: $-0.34 - Hong Kong property developer's recovery trajectory will indicate broader Chinese real estate market sentiment.

• Iperionx Ltd. (IPX) at 13:00 BST [Pre-Market] - Est: $-0.00 vs Prev: $-0.01 - Critical minerals producer's performance reflects supply chain resilience in strategic materials sector.

• Deep Yellow Limited (DYL) at 13:00 BST [Pre-Market] - Est: $-0.00 vs Prev: $-0.00 - Uranium developer's results will impact nuclear energy investment themes amid global energy transition.

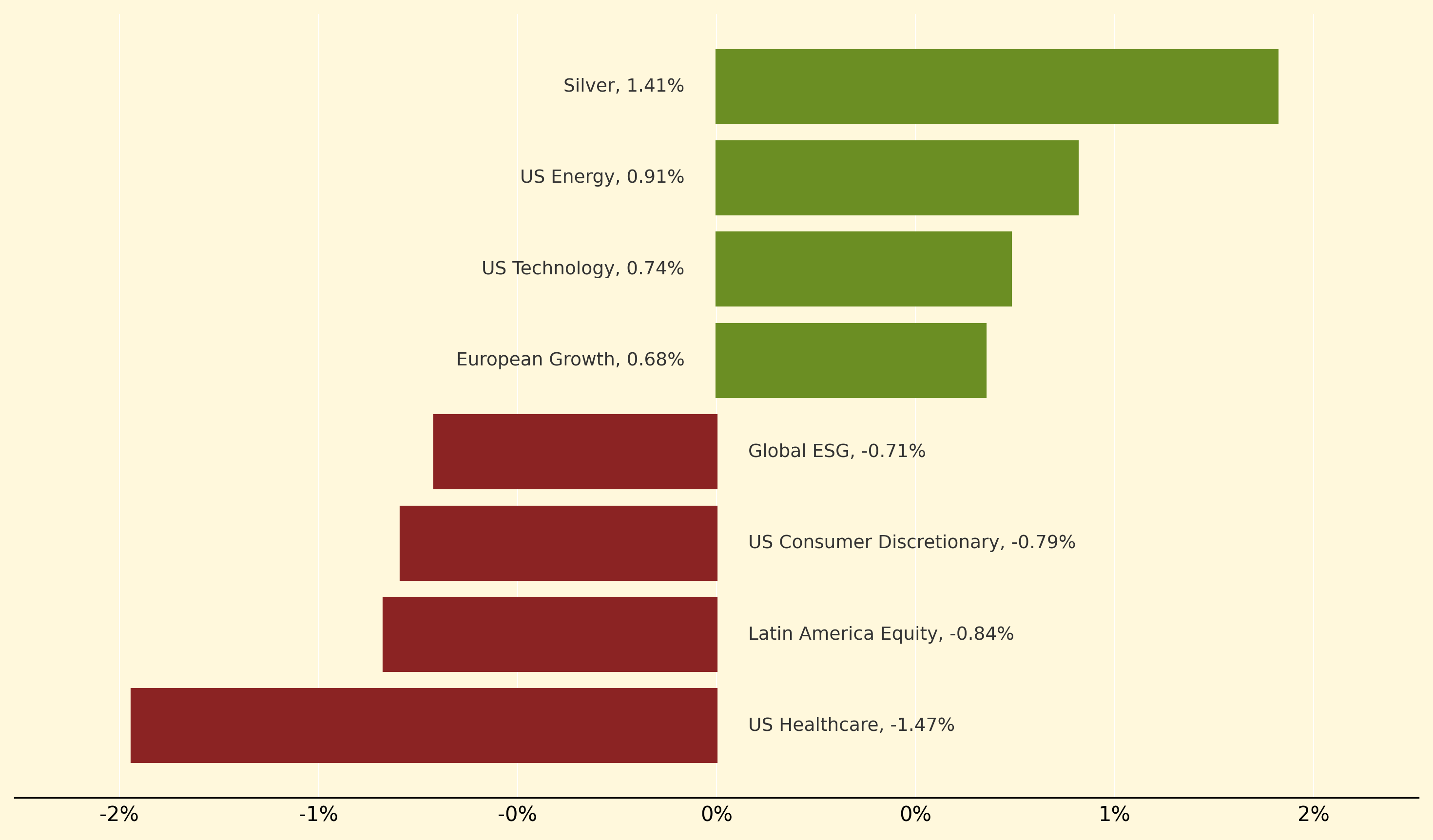

Silver surged 1.41% to lead commodity gains as Russian energy export restrictions and geopolitical tensions drove precious metals demand, while US Energy climbed 0.91% benefiting directly from oil's strongest weekly performance in three months. US Technology advanced 0.74% despite broader market weakness, showing resilience amid the sector-specific tariff announcements that targeted pharmaceuticals rather than tech infrastructure.

US Healthcare suffered the steepest decline at -1.47% as Trump's 100% tariffs on branded pharmaceuticals sent shockwaves through the sector, forcing immediate supply chain recalculations for multinational drug manufacturers. Latin America Equity dropped 0.84% amid emerging market pressure from the renewed tariff escalation, while US Consumer Discretionary fell 0.79% as strong GDP data and falling jobless claims reduced expectations for aggressive Fed easing from 125 to 100 basis points through year-end.

Bond Vigilantes: Investors who aggressively sell government bonds to protest fiscal irresponsibility, forcing yields higher and constraining government spending through market discipline rather than political processes, particularly threatening for heavily indebted nations.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry