Fed Delivers Dovish Cut Amid Labour Market Shift | Links: [1], [2], [3]

The Federal Reserve reduced rates by 25 basis points to the 4.50-4.75% range yesterday, marking its first reduction of 2025 and signalling two additional cuts ahead despite persistent inflation concerns. Chair Jerome Powell characterised the move as "risk management" rather than aggressive easing, citing a jobs market that is "no longer very solid" as the primary driver. The Fed's dot plot projects further reductions even as core inflation remains elevated, creating a complex policy backdrop that disappointed markets expecting more dovish signals. Trump appointee Michelle Bowman dissented, preferring no change and highlighting internal divisions. Treasury yields rose and equities posted mixed reactions as Powell explicitly pushed back against expectations for 50bp cuts, emphasising the Fed's cautious, data-dependent approach. The measured stance creates significant cross-asset volatility as markets recalibrate expectations for the easing cycle ahead.

China Escalates Nvidia Restrictions as US-China Tech War Intensifies | Links: [4], [5], [6]

China ordered domestic companies to halt all purchases of Nvidia's AI chips yesterday, including repurposed models designed to comply with US export controls, representing another escalation in the technology trade conflict. The directive affects Nvidia's attempts to maintain Chinese market access through modified chip designs, with CEO Jensen Huang expressing disappointment whilst stating the company "won't operate where we're not wanted." The timing coincides with Huawei unveiling new AI chip technology to rival Nvidia's offerings, demonstrating China's accelerated push for semiconductor self-sufficiency. Chinese tech stocks rallied on the news as domestic AI companies benefit from reduced competition, whilst the restrictions create immediate headwinds for Nvidia's revenue prospects in what was a crucial market. The escalation reinforces supply chain diversification themes and may accelerate Western investment in alternative chip architectures outside China.

Trump's UK State Visit Yields £150bn Investment Package | Links: [7]

President Trump's state visit to Britain resulted in £150bn ($205bn) in US investment commitments, including Nvidia's £11bn AI programme and GSK's $30bn pharmaceutical expansion. The visit featured full royal pageantry with King Charles hosting the president, underscoring the diplomatic importance of the US-UK relationship amid broader geopolitical tensions. The investments span technology, pharmaceuticals, and defence sectors, with particular emphasis on artificial intelligence capabilities that position Britain as a strategic partner in America's tech competition with China. The magnitude represents one of the largest bilateral investment packages in recent memory, supporting sterling and UK growth prospects whilst strengthening transatlantic economic ties. The substantial capital commitments could drive sustained inflows to UK markets, though deployment timelines and project conditionality remain key factors for sustained market impact.

Asian Markets Hit Records as Policy Easing Fuels EM Optimism | Links: [8], [9], [10]

Japanese equities reached fresh records whilst Asian emerging markets rallied broadly on Fed easing prospects and regional central bank policy flexibility. The Nikkei's historic highs came ahead of the Bank of Japan's policy meeting, where rates are expected to remain steady despite potential October signals for tightening. Fund managers are showing their highest optimism since February, with increased allocations to India and South Korea driving regional outperformance. The Bank of Canada added to the global easing narrative with a 25bp cut to 2.50%, citing GDP contraction of 1.5% in Q2 amid trade uncertainty. However, the dollar's post-Fed strength threatens to weigh on Asian currencies going forward, creating potential headwinds for the broader regional rally as divergent central bank policies across the region require tactical positioning adjustments within Asian allocations.

Ex-BoE Deputy Warns of US Payment System Weaponisation Risks | Links: [11], [12]

Former Bank of England deputy governor Sir Dave Ramsden warned that the Trump administration could weaponise US payment systems by activating "kill switches" for Visa and Mastercard networks, potentially freezing global financial transactions at will. The threat extends to Federal Reserve dollar swap lines, which could be terminated to pressure foreign central banks, highlighting the systemic vulnerability of dollar-dominated international payment infrastructure to political manipulation. These warnings gain urgency as Trump has already moved to challenge Fed independence through attempts to fire Governor Lisa Cook and appointments like Michelle Bowman who dissented on rate policy yesterday. Such weaponisation could fundamentally reshape international finance, forcing development of alternative payment systems and potentially accelerating de-dollarisation trends among major economies. The systemic threat creates new risk premiums for dollar-dependent payment flows whilst reinforcing the importance of operational resilience planning for global financial institutions.

| Dow Jones Industrial Average | --▲ +0.52% |

| S&P 500 | --▼ -0.07% |

| Hang Seng Index | --▲ +1.33% |

| FTSE 100 | --▲ +0.14% |

| CAC 40 | --▼ -0.70% |

| DAX 40 | --▼ -0.21% |

| Euro Stoxx 50 | --▼ -0.22% |

| Nasdaq Composite | --▼ -0.32% |

| Nasdaq-100 | --▼ -0.26% |

| Nikkei 225 | --▲ +0.09% |

| S&P/ASX 200 | --▼ -0.67% |

| Shanghai Composite | --▲ +0.58% |

| S&P 500 E-mini | 6690.00+31.25▲ +0.47% |

| Nasdaq-100 | 24631.80+166.50▲ +0.68% |

| FTSE 100 Index | 9276.00+12.00▲ +0.13% |

| EURO STOXX 50 | 5389.00+22.00▲ +0.41% |

| WTI Crude Oil | 63.44-0.26▼ -0.41% |

| Gold (COMEX) | 3692.10-25.70▼ -0.69% |

| Copper (COMEX) | 4.61-0.03▼ -0.58% |

| US 10-Year Treasury | 113.22+0.09▲ +0.08% |

| UK Long Gilt (10Y) | 117.94+0.00▲ +0.00% |

| German Bund (10Y) | 128.87-0.04▼ -0.03% |

| Italian BTP (10Y) | 120.34+0.17▲ +0.14% |

| US Dollar Index | 96.83+0.20▲ +0.20% |

| VIX Volatility | 17.50-0.28▼ -1.57% |

| SONIA 3M Interest Rate | 96.14+0.00▼ -0.01% |

• GB BoE Interest Rate Decision at 12:00 BST - Forecast: 4.0% vs Previous: 4.0% - Key policy decision that will drive GBP volatility and signal the Bank's stance on inflation and economic growth.

• JP Inflation Rate YoY at 00:30 BST (Friday) - Previous: 3.1% - Critical gauge of Japan's price pressures that could influence BoJ policy expectations and JPY direction.

• GB BoE MPC Vote Unchanged at 12:00 BST - Forecast: 8.0 vs Previous: 4.0 - Indicates growing consensus among policymakers for holding rates steady, signalling dovish shift in monetary policy stance.

• GB BoE MPC Vote Cut at 12:00 BST - Forecast: 1.0 vs Previous: 5.0 - Shows declining support for rate cuts among MPC members, reflecting improved inflation outlook and economic resilience.

• US Initial Jobless Claims at 13:30 BST - Forecast: 240K vs Previous: 263K - Weekly employment indicator that could influence Fed policy expectations and USD strength amid ongoing labour market assessment.

• US Philadelphia Fed Manufacturing Index at 13:30 BST - Forecast: 3.0 vs Previous: -0.3 - Regional manufacturing gauge that signals broader industrial health and potential Fed policy implications.

• Next plc (NXT) at 07:00 GMT [Pre-Market] - Est: $4.41 vs Prev: $4.42 - UK retail bellwether's performance will signal consumer spending trends across European fashion markets.

• Darden Restaurants, Inc. (DRI) at 12:00 GMT [Pre-Market] - Est: $2.00 vs Prev: $2.98 - Restaurant sector earnings may indicate consumer discretionary strength amid inflationary pressures.

• Allegro.eu SA (ALE) at 13:00 GMT [Pre-Market] - Est: $0.25 vs Prev: $0.19 - Central European e-commerce leader's results could impact broader European tech and retail sectors.

• FactSet Research Systems Inc. (FDS) at 14:30 GMT [During-Hours] - Est: $4.13 vs Prev: $4.27 - Financial data provider's guidance will reflect institutional investment demand and fintech sector health.

• FedEx Corporation (FDX) at 21:00 GMT [During-Hours] - Est: $3.65 vs Prev: $6.07 - Logistics giant's performance serves as key economic indicator for global trade and shipping volumes.

• Lennar Corporation (LEN) at 21:00 GMT [During-Hours] - Est: $2.10 vs Prev: $1.81 - Major homebuilder's results will signal US housing market strength and construction sector outlook.

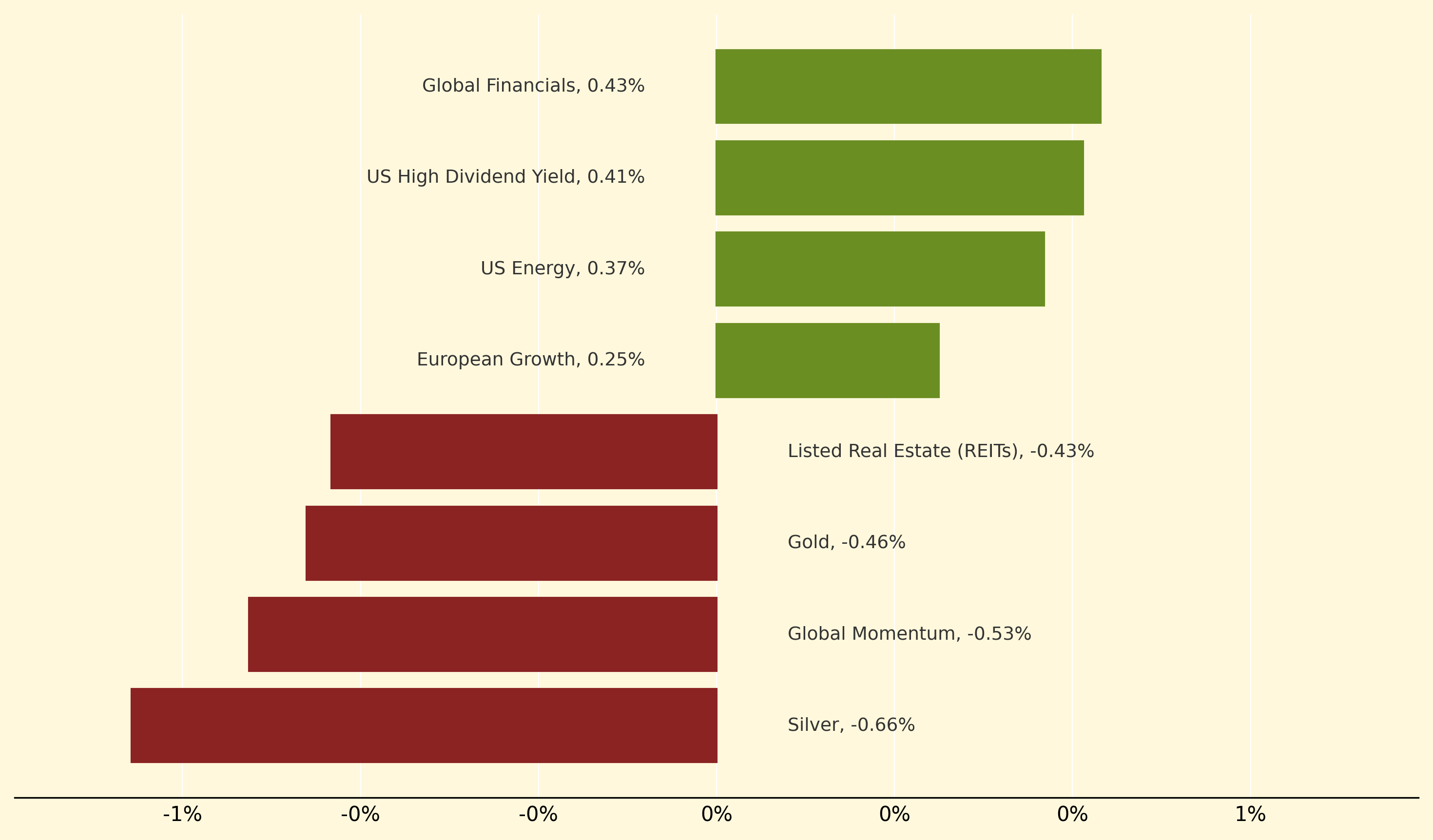

Global Financials led yesterday's gains, climbing 0.43% as the Fed's dovish 25bp rate cut and signals for further easing boosted banking sector sentiment despite Powell's cautious tone. US High Dividend Yield strategies also performed well, advancing 0.41%, whilst US Energy rose 0.37% amid broader market optimism following the policy shift.

Conversely, precious metals underperformed significantly, with Silver dropping 0.66% and Gold falling 0.46% as the dollar strengthened following Powell's measured commentary that disappointed markets expecting more aggressive easing signals. Global Momentum strategies also lagged, declining 0.53%, whilst Listed Real Estate (REITs) fell 0.43% as rising Treasury yields pressured interest-sensitive sectors despite the rate cut.

Dollar swap lines: Bilateral agreements between the Federal Reserve and foreign central banks that provide emergency dollar liquidity during financial stress, serving as crucial backstops for global dollar funding markets and international monetary system stability.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry