Fed Decision Day: Dollar Weakness and Record Gold Signal Monetary Pivot | Links: [1], [2], [3]

The dollar has declined to four-year lows against the euro at 1.1867 as markets position for today's widely expected 25 basis point Fed rate cut - the first move in what traders anticipate could be 150 basis points of easing through next year. Gold has climbed past $3,700 to fresh records, marking a notable 41% gain this year as investors seek inflation hedges ahead of the monetary pivot. Treasury Secretary Bessent's public endorsement of James Bullard for Fed Chair adds another layer of uncertainty, particularly given Bullard's comments about defending dollar reserve status and potential future rate hikes. Perhaps most striking is that foreign investors are now hedging 80% of their US equity flows, the highest level on record, indicating fundamental shifts in how global capital views American assets. The focus has shifted from the rate cut itself to Powell's forward guidance and the quarterly dot plot.

Supreme Court Tariff Case Threatens $100bn Market Disruption | Links: [4], [5], [6]

Wall Street and Corporate America are bracing for potential disruption as the Supreme Court prepares to hear a landmark case challenging the constitutionality of presidential tariff powers. The case could trigger up to $100 billion in refunds to affected companies and reshape US trade policy architecture. This comes as Treasury Secretary Bessent signals optimism for a China trade deal before November's reciprocal tariff deadline, while Asian fund managers warn that the region's record stock rally may unravel as tariff impacts intensify. Japan's exports have declined for four consecutive months, with US shipments falling particularly sharply, highlighting the real economic damage from trade tensions. The legal uncertainty creates policy risk affecting everything from corporate earnings to international supply chains.

Tech Giants Pledge $42bn to UK AI Infrastructure | Links: [7], [8], [9]

Major US technology companies have committed over $42 billion to UK artificial intelligence infrastructure, with Microsoft leading a £22 billion investment as part of President Trump's state visit. Google separately announced a £5 billion AI commitment, while other tech giants joined the initiative spanning quantum computing, data centres, and AI research facilities. This substantial capital commitment positions the UK as a key technology hub post-Brexit and contrasts sharply with Chinese tech stocks surging to four-year highs on their own AI optimism - Baidu soared 16% to two-year highs after securing new AI partnerships. This transatlantic tech investment surge comes as China's tightening grip on rare earth exports continues to cost European tech companies "millions of euros" in production disruptions despite recent diplomatic progress.

UBS Reviews All Options Including HQ Relocation Over Swiss Capital Rules | Links: [10]

UBS is considering all strategic options, including potential headquarters relocation, in response to Swiss proposals for significantly higher capital requirements. The systemically important bank's CFO indicated that all alternatives remain under consideration as regulators seek to address "too big to fail" concerns in the Swiss market. This unprecedented threat by a major global bank to relocate its headquarters over regulatory constraints represents a new escalation in the ongoing tension between financial institutions and post-crisis regulatory frameworks. The move could prompt a broader reassessment of regulatory competitiveness among major financial centres, particularly as other European banks face similar pressures from their respective regulators.

Energy Security Tensions Rise as Ukraine Targets Russian Infrastructure | Links: [11], [12], [13]

Ukrainian drone strikes on Russian oil infrastructure, including the Saratov refinery with capacity of 300,000 barrels per day, have pushed oil prices over 1% higher and added geopolitical risk premiums to energy markets. This escalation occurs as the International Energy Agency warns of accelerating decline rates in global oil and gas field output, requiring $540 billion annually in new exploration investment to maintain supply. The energy security implications extend beyond commodities - European industrial output remains weak partly due to energy cost pressures, while the Netherlands has committed €27 billion to defence spending to meet NATO's 5% GDP target. These developments underscore how geopolitical tensions are reshaping both energy markets and fiscal priorities.

| Dow Jones Industrial Average | --▼ -0.35% |

| S&P 500 | --▼ -0.26% |

| Hang Seng Index | --▼ -0.37% |

| FTSE 100 | --▼ -0.88% |

| CAC 40 | --▼ -0.92% |

| DAX 40 | --▼ -1.61% |

| Euro Stoxx 50 | --▼ -1.24% |

| Nasdaq Composite | --▼ -0.28% |

| Nasdaq-100 | --▼ -0.28% |

| Nikkei 225 | --▼ -0.10% |

| S&P/ASX 200 | --▲ +0.28% |

| Shanghai Composite | --▼ -0.11% |

| S&P 500 E-mini | 6664.50-3.00▼ -0.04% |

| Nasdaq-100 | 24514.20-8.00▼ -0.03% |

| FTSE 100 Index | 9212.50+8.50▲ +0.09% |

| EURO STOXX 50 | 5386.00+14.00▲ +0.26% |

| WTI Crude Oil | 64.42-0.10▼ -0.15% |

| Gold (COMEX) | 3717.70-7.40▼ -0.20% |

| Copper (COMEX) | 4.66-0.03▼ -0.64% |

| US 10-Year Treasury | 113.55+0.00▲ +0.00% |

| UK Long Gilt (10Y) | 117.94+0.03▲ +0.03% |

| German Bund (10Y) | 128.79+0.08▲ +0.06% |

| Italian BTP (10Y) | 120.17-0.09▼ -0.07% |

| US Dollar Index | 96.31+0.05▲ +0.05% |

| VIX Volatility | 18.36-0.09▼ -0.49% |

| SONIA 3M Interest Rate | 96.03+0.00▲ +0.00% |

• UK Inflation Rate YoY at 07:00 BST - Forecast: 3.9% vs Previous: 3.8% - Key data for BoE policy expectations as inflation remains above target, likely to impact GBP and gilt yields.

• Canada BoC Interest Rate Decision at 14:45 BST - Forecast: 2.5% vs Previous: 2.75% - Expected 25bp cut could weaken CAD and signal continued easing cycle amid economic softening.

• US Fed Interest Rate Decision at 19:00 BST - Forecast: 4.25% vs Previous: 4.5% - Anticipated 25bp cut will drive USD moves and global risk sentiment as markets assess Fed's dovish pivot.

• US FOMC Economic Projections at 19:00 BST - Updated dot plot and growth forecasts will shape 2025 rate expectations and influence Treasury yields across the curve.

• US Fed Press Conference at 19:30 BST - Powell's commentary on inflation progress and employment outlook crucial for market positioning ahead of year-end.

• UK Core Inflation Rate YoY at 07:00 BST - Forecast: 3.7% vs Previous: 3.8% - Services inflation remains BoE's key concern for underlying price pressures and wage-price spiral risks.

• Barratt Redrow plc (BTRW) at 07:00 GMT Pre-Market - Est: TBD vs Prev: $0.11 - UK housebuilder results will signal residential property market health amid ongoing mortgage rate pressures.

• General Mills, Inc. (GIS) at 12:00 GMT Pre-Market - Est: $0.81 vs Prev: $0.74 - Consumer staples giant's performance indicates resilience of defensive sectors and inflationary cost management.

• EXOR N.V. (EXO) at 13:00 GMT Pre-Market - Est: TBD vs Prev: $71.75 - Agnelli family's investment holding company results reflect broader European industrial and luxury goods exposure.

• Bollore SE (BOL) at 13:00 GMT Pre-Market - Est: TBD vs Prev: $0.03 - French conglomerate's logistics and media divisions provide insight into European industrial activity and African market exposure.

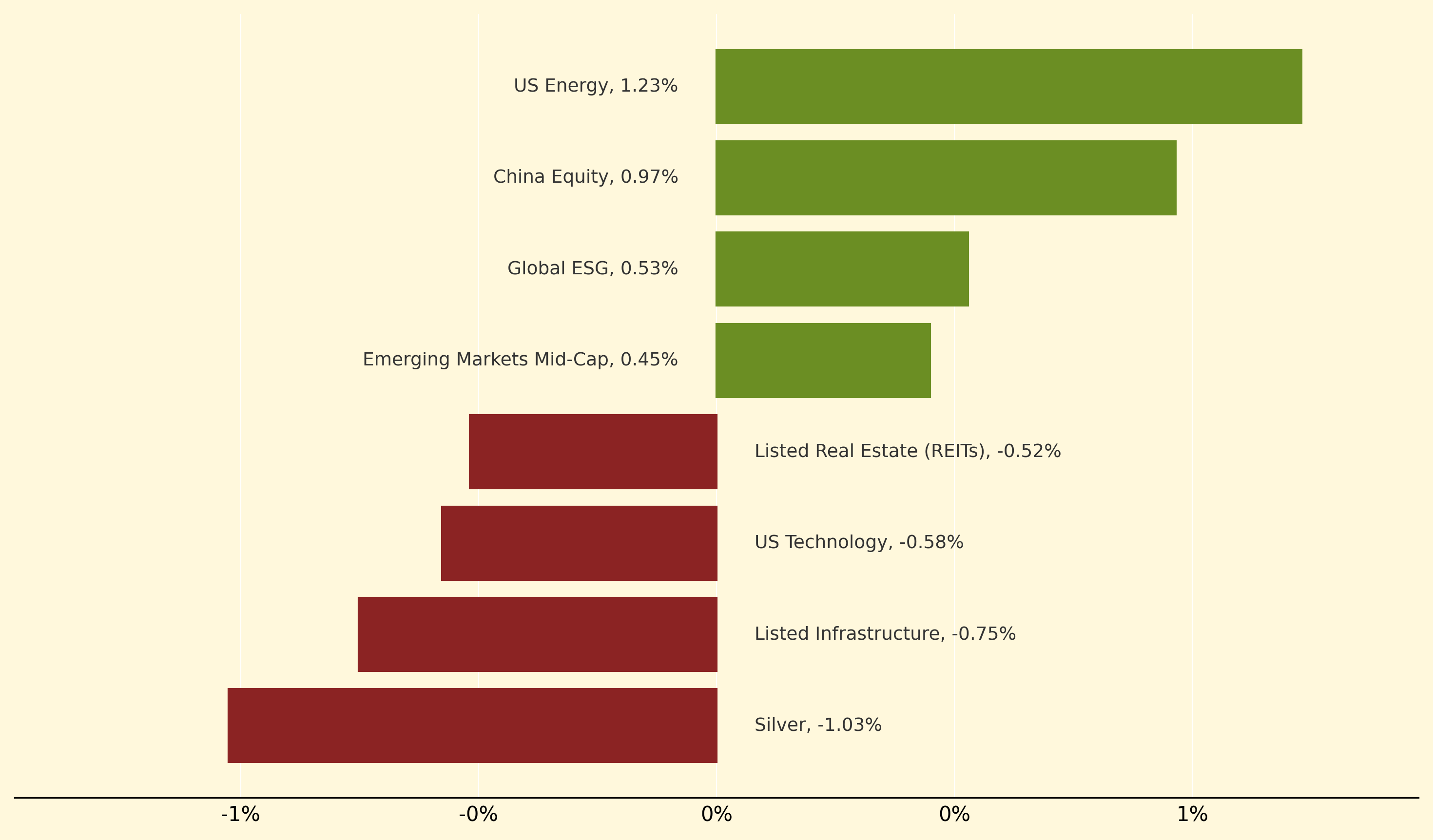

US Energy led yesterday's gains, climbing 1.23% as Ukrainian strikes on Russian oil infrastructure sent crude prices over 1% higher and added geopolitical risk premiums to energy markets. China Equity also performed well, advancing 0.97% amid broader Asian optimism, with Chinese tech stocks reaching four-year highs on AI partnership announcements and Baidu soaring 16% to two-year peaks.

Conversely, Silver underperformed significantly, dropping 1.03% as investors rotated toward record-breaking gold positions above $3,700. US Technology also lagged, falling 0.58% despite substantial UK AI investment commitments from Microsoft and Google, while Listed Infrastructure declined 0.75% and REITs dropped 0.52% as higher rate cut expectations pressured yield-sensitive sectors ahead of the Fed decision.

Dot Plot: A quarterly chart published by the Federal Reserve showing each FOMC member's anonymous projection for the federal funds rate over the next three years. Markets scrutinise these interest rate forecasts heavily as they signal the central bank's collective thinking on monetary policy trajectory, often moving bond and currency markets more than the actual rate decision itself.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry