Global Central Bank Coordination Week Approaches | Links: [1], [2], [3]

Central banks controlling half the world's most-traded currencies will announce policy decisions within 36 hours this week, marking the Fed's first rate cut of 2025 as the centrepiece of an extraordinary monetary coordination moment. Markets have crystallised around a 25bp Fed cut with 71bps of easing priced by Christmas, supported by 105 of 107 economists expecting action. Yet policy divergence is accelerating: the ECB has paused its easing cycle with officials like Dr. Joachim Nagel warning against further cuts, the Bank of Japan is expected to hold steady, and the Bank of England faces inflation expectations at two-year highs. Trump's public pressure for a "big cut" and threats to Fed independence add complexity amid impending currency realignments.

China's Economic Deterioration Deepens with Worst Data in a Year | Links: [4], [5], [6]

China's August economic data revealed a broad-based collapse that exceeded economists' worst fears, with industrial output growing just 4.5% year-on-year against 5.1% expected and retail sales slumping to 2.1% versus 2.5% forecasted. The property crisis intensified with new construction starts down 19.5% year-to-date and home prices accelerating their decline despite expanded government support measures. Credit expansion has slowed to record lows as borrowing demand evaporates, while youth unemployment resurges and BYD suffered £35 billion in market cap destruction amid brutal EV sector price wars. The deterioration casts serious doubt on China's 5% growth target and raises expectations for emergency stimulus measures, with HSBC's chief economist warning of persistent investment headwinds that could reshape global commodity demand.

France Faces Worst Credit Rating as Sovereign Risk Returns to Europe | Links: [7], [8], [9]

Fitch downgraded France to A+, its lowest rating on record, citing political instability and the eurozone's highest budget deficit under Michel Barnier's fragile coalition government. The move comes as French corporate bonds now trade through sovereign yields, an alarming risk premium inversion that signals market concern over the state's fiscal trajectory. France could also face up to €4 billion of additional costs from Bank of England gilt decisions, all while navigating political issues that threaten fiscal consolidation. This sovereign stress emerges as the EU delays its 2040 climate targets following German-backed French concerns over economic competitiveness, creating dangerous precedent for potential contagion to other peripheral eurozone members already struggling with elevated debt levels.

US-China Trade Negotiations Resume with TikTok Deal on the Horizon | Links: [10], [11]

US-China talks in Spain are progressing toward a potential TikTok resolution, with Treasury Secretary Bessent declaring the countries are "close to a TikTok deal" alongside broader trade concession discussions. The negotiations represent a significant thaw in bilateral relations after months of escalating tensions, with both sides showing renewed willingness to engage on technology transfers, market access, and regulatory frameworks. The TikTok resolution could serve as a template for addressing other US technology security concerns while preserving commercial relationships, providing relief as US companies report severe impacts from existing tariffs regarding job cuts and margin pressure.

US Market Euphoria Faces £5.5 Trillion Liquidity Test as Rate Cuts Begin | Links: [12], [13], [14]

US equity markets achieved record highs with the S&P 500 and Nasdaq posting new peaks, but a massive £5.5 trillion "wall of cash" in money market funds could reshape asset allocation as Fed cuts reduce money market yields. This liquidity stockpile, built during the high-rate environment, faces imminent redeployment while global equity funds recorded their first weekly outflows in five weeks totalling £2.4 billion despite record market levels. The AI trade has shown renewed strength following Oracle's 36% surge on OpenAI partnerships, yet market concentration concerns mount with AI companies comprising 30% of S&P 500 weight. Technical risks emerge as Wall Street braces for quarter-end funding stress, creating a complex backdrop where record equity valuations meet a significant cash reallocation.

| Dow Jones Industrial Average | --▼ -0.53% |

| S&P 500 | --▼ -0.10% |

| Hang Seng Index | --▼ -0.57% |

| FTSE 100 | --▼ -0.15% |

| CAC 40 | --▼ -0.07% |

| DAX 40 | --▼ -0.29% |

| Euro Stoxx 50 | --▲ +0.07% |

| Nasdaq Composite | --▲ +0.28% |

| Nasdaq-100 | --▲ +0.26% |

| Nikkei 225 | --▼ -0.08% |

| S&P/ASX 200 | --▲ +0.68% |

| Shanghai Composite | --▼ -0.13% |

| S&P 500 E-mini | 6610.25+22.00▲ +0.33% |

| Nasdaq-100 | 24176.00+62.75▲ +0.26% |

| FTSE 100 Index | 9293.50-2.00▼ -0.02% |

| EURO STOXX 50 | 5429.00+41.00▲ +0.76% |

| WTI Crude Oil | 63.21+0.52▲ +0.83% |

| Gold (COMEX) | 3690.10+3.70▲ +0.10% |

| Copper (COMEX) | 4.67+0.02▲ +0.45% |

| US 10-Year Treasury | 113.44+0.16▲ +0.14% |

| UK Long Gilt (10Y) | 117.90+0.08▲ +0.07% |

| German Bund (10Y) | 128.71+0.15▲ +0.12% |

| Italian BTP (10Y) | 120.17+0.25▲ +0.21% |

| US Dollar Index | 96.95-0.20▼ -0.20% |

| VIX Volatility | 17.78-0.16▼ -0.93% |

| SONIA 3M Interest Rate | 96.03+0.01▲ +0.01% |

• UK Unemployment Rate (Tuesday, 07:00 BST) - Forecast: 4.7% vs Previous: 4.7% - Key labour market indicator affecting BoE policy decisions and GBP volatility.

• German ZEW Economic Sentiment Index (Tuesday, 10:00 BST) - Forecast: 25.0 vs Previous: 34.7 - Critical gauge of German economic confidence impacting EUR and European equity markets.

• Canadian Inflation Rate YoY (Tuesday, 13:30 BST) - Previous: 1.7% - Crucial for BoC policy ahead of Wednesday's rate decision, affecting CAD positioning.

• US Retail Sales MoM (Tuesday, 13:30 BST) - Forecast: 0.3% vs Previous: 0.5% - Key consumer spending indicator influencing Fed policy expectations and USD strength.

• Japanese Balance of Trade (Wednesday, 00:50 BST) - Forecast: ¥-513.6B vs Previous: ¥-118.4B - Significant deterioration expected, impacting JPY and trade sentiment.

• UK Inflation Rate YoY (Wednesday, 07:00 BST) - Forecast: 3.9% vs Previous: 3.8% - Critical for BoE rate path with decision following day, affecting GBP and gilt yields.

• Canadian BoC Interest Rate Decision (Wednesday, 14:45 BST) - Forecast: 2.50% vs Previous: 2.75% - Expected 25bp cut following weak inflation data, major CAD market mover.

• US Fed Interest Rate Decision (Wednesday, 19:00 BST) - Forecast: 4.25% vs Previous: 4.50% - Anticipated 25bp cut with economic projections, pivotal for USD and global risk sentiment.

• UK BoE Interest Rate Decision (Thursday, 12:00 BST) - Forecast: 4.00% vs Previous: 4.00% - Hold expected but voting split crucial for future policy direction and GBP.

• Japanese BoJ Interest Rate Decision (Friday, 04:00 BST) - Forecast: 0.50% vs Previous: 0.50% - Hold expected but any hawkish signals could strengthen JPY significantly.

• UK Retail Sales MoM (Friday, 07:00 BST) - Forecast: 0.2% vs Previous: 0.6% - Important consumer spending data following BoE decision, affecting UK growth outlook.

• Ferguson Enterprises (FERG) - Tuesday, 11:45 BST - Pre-Market - $41.7B - Leading plumbing and heating distributor serving as key indicator for US construction and infrastructure spending trends.

• FedEx Corporation (FDX) - Thursday, 21:00 BST - During-Hours - $54.2B - Global logistics bellwether providing crucial insights into international trade flows and e-commerce demand patterns.

• Lennar Corporation (LEN) - Thursday, 21:00 BST - During-Hours - $35.4B - Major US homebuilder offering key data on housing market health amid interest rate environment concerns.

• EXOR N.V. (EXO) - Wednesday, 13:00 BST - Pre-Market - $31.5B - Agnelli family investment vehicle with stakes in Ferrari, Stellantis, and CNH Industrial, reflecting European automotive sector performance.

• General Mills (GIS) - Wednesday, 12:00 BST - Pre-Market - $26.7B - Consumer staples giant providing insights into inflation impact on food costs and consumer spending resilience.

• Darden Restaurants (DRI) - Thursday, 12:00 BST - Pre-Market - $24.8B - Olive Garden parent company serving as key indicator for US consumer discretionary spending and restaurant industry health.

• Next plc (NXT) - Thursday, 07:00 BST - Pre-Market - $19.0B - FTSE 100 retail heavyweight offering crucial insights into UK consumer confidence and high street performance.

• Bollore SE (BOL) - Wednesday, 13:00 BST - Pre-Market - $16.0B - French conglomerate with significant logistics and media operations across Europe and Africa markets.

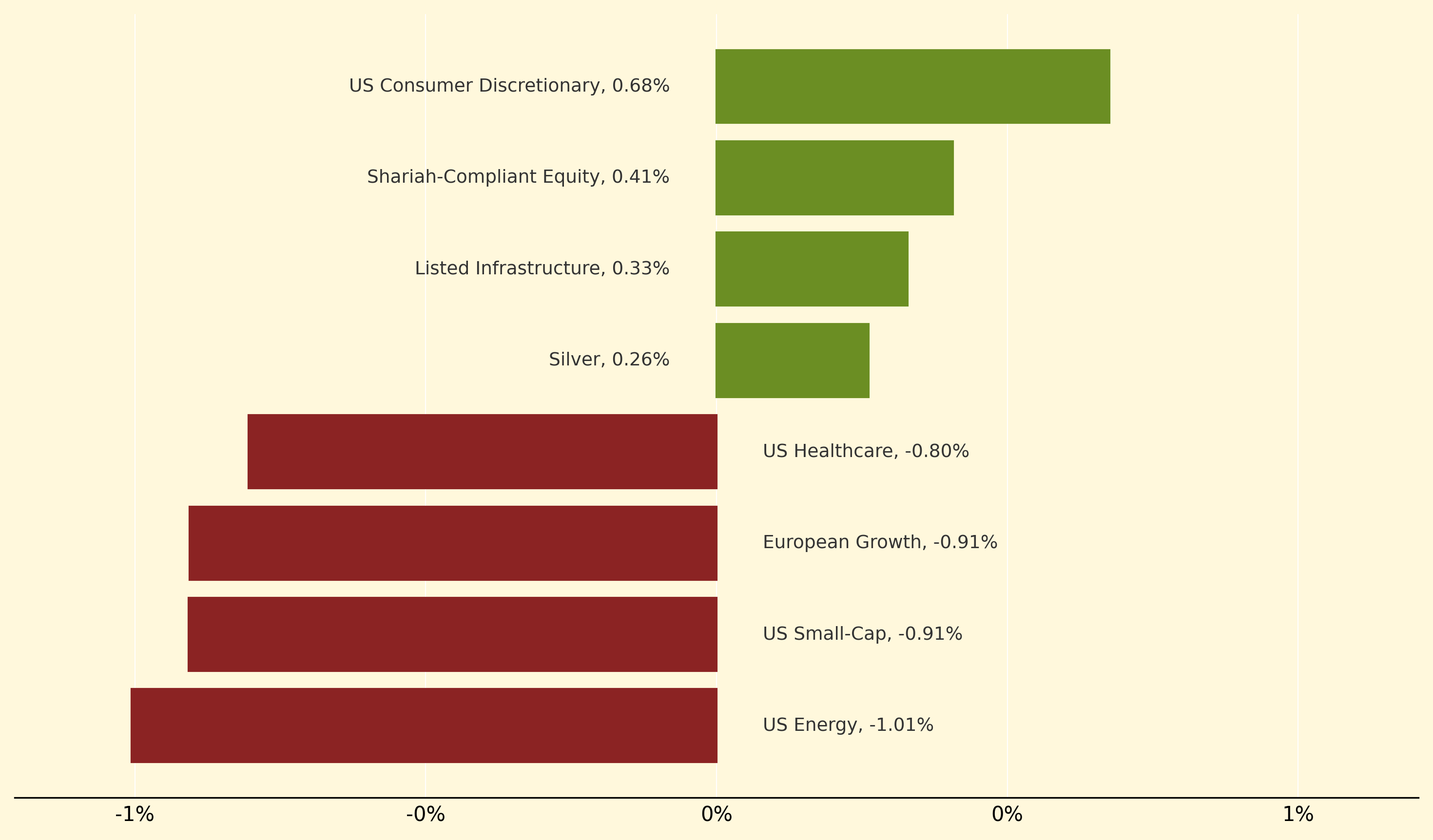

US Consumer Discretionary led market gains with a 0.68% advance as investors positioned for potential Fed rate cuts that could boost consumer spending power. Shariah-Compliant Equity and Listed Infrastructure also outperformed, rising 0.41% and 0.33% respectively, reflecting defensive positioning ahead of central bank decisions and infrastructure investment themes gaining traction amid policy uncertainty.

US Energy suffered the steepest decline at -1.01% as oil demand concerns weighed on the sector despite ongoing Ukrainian attacks on Russian facilities. US Small-Cap and European Growth both fell 0.91%, with smaller companies particularly vulnerable to economic slowdown fears highlighted by China's deteriorating August data. US Healthcare dropped 0.80%, potentially reflecting sector rotation away from defensive plays as rate cut expectations solidified.

Risk premium inversion: A dangerous market anomaly where corporate bonds trade at lower yields than government debt, signalling investors view private companies as safer than the sovereign state—typically indicating severe concerns about government fiscal stability and creditworthiness.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry