Global Equity Markets Hit Records as Disinflationary Data Fuels Rate Cut Euphoria | Links: [1], [2], [3]

A wave of record-breaking performances swept global equity markets as unexpected US producer price declines turbocharged Fed rate cut expectations. The S&P 500 closed at consecutive records while Asian markets followed suit, with Japan's Nikkei hitting new highs and South Korea's Kospi reaching record levels. The catalyst was August PPI data showing wholesale prices falling 0.1% versus expectations for a flat reading—the first drop since April. Oracle's surge on massive AI growth projections lifted the entire technology complex, with Nvidia, Broadcom, and TSMC rallying in sympathy. Traders are now pricing in more aggressive Fed easing scenarios ahead of today's crucial CPI data, with the disinflationary signal reinforcing market conviction that monetary policy will turn sharply dovish.

China Considers $1 Trillion Local Government Debt Relief Package | Links: [4]

Beijing is mulling a massive $1 trillion intervention to address mounting local government debt burdens, representing one of the largest fiscal support measures in the country's recent history. The unprecedented scale highlights Beijing's growing concerns about sub-sovereign debt sustainability and its potential impact on the broader economy. This package would dwarf previous stimulus measures and signals China's willingness to deploy significant fiscal resources to maintain economic stability. The timing coincides with Chinese government bond yields reaching 2025 highs, suggesting market recognition of shifting fiscal dynamics. The intervention reflects both the severity of local government debt stress and China's commitment to preventing a systemic crisis that could destabilise the world's second-largest economy.

Bank of Japan Rate Hike Expected by January as Inflation Accelerates | Links: [5], [6]

Bank of Japan watchers anticipate a rate hike by January 2025, with 36% predicting an October move, as wholesale inflation accelerated in August to signal building price pressures. This hawkish turn creates a remarkable three-way policy divergence among major central banks, with the Fed cutting aggressively, the ECB holding steady, and the BOJ preparing to tighten. Japanese wholesale prices rising faster than expected adds urgency to BOJ deliberations about the appropriate pace of policy normalisation. The timing coincides with potential Fed cuts, reshaping global carry trade dynamics and cross-currency flows. This divergence presents complex opportunities across fixed income and foreign exchange markets as traditional monetary policy coordination breaks down.

European Central Bank Holds Firm as Economy Weathers Trade War Storm | Links: [7], [8], [9]

The European Central Bank is expected to hold rates at 2% today, with market watchers suggesting the cutting cycle may have ended as the eurozone economy demonstrates resilience against Trump tariff threats. This hawkish pivot contrasts sharply with Fed dovishness, creating potential currency and policy divergence opportunities. France faces additional challenges beyond political turmoil, with potential credit rating downgrades looming and new Prime Minister Michel Barnier confronting immediate protests while promising budget cuts and debt reduction. Meanwhile, the UK services sector is helping soften the Brexit and tariff impact, though property tax uncertainty continues to dampen housing market activity. The ECB-Fed policy split creates substantial cross-currency opportunities while French political risk adds complexity to eurozone periphery strategies.

Geopolitical Flashpoints Test Market Resilience Amid Policy Divergence | Links: [10], [11], [12]

Beneath the surface of record equity highs, serious geopolitical tensions are escalating with Poland shooting down Russian drones in the first direct NATO-Russia military contact since the Ukraine invasion began. The incident triggered defence stock rallies across Europe and lifted oil prices above $1 per barrel. An 'anti-Western alliance' of China, Russia, and North Korea is raising concerns about a new axis of global power, while the assassination of Trump ally Charlie Kirk represents a dangerous escalation in US political violence. These developments test market resilience and highlight the fragility of the current risk-on environment, particularly as central banks pursue divergent policies and trade wars intensify. The combination of monetary policy divergence and geopolitical stress creates both complex cross-asset opportunities and significant tail risks that could quickly reverse current market euphoria.

| Dow Jones Industrial Average | --▼ -0.53% |

| S&P 500 | --▼ -0.28% |

| Hang Seng Index | --▲ +0.61% |

| FTSE 100 | --▼ -0.19% |

| CAC 40 | --▼ -0.17% |

| DAX 40 | --▼ -0.86% |

| Euro Stoxx 50 | --▼ -0.48% |

| Nasdaq Composite | --▼ -0.43% |

| Nasdaq-100 | --▼ -0.34% |

| Nikkei 225 | --▲ +0.75% |

| S&P/ASX 200 | --▲ +0.31% |

| Shanghai Composite | --▲ +0.15% |

| S&P 500 E-mini | 6549.00-- |

| Nasdaq-100 Futures | 23934.20-- |

| FTSE 100 Index Futures | 9279.00-- |

| EURO STOXX 50 Futures | 5371.00-- |

| US Dollar Index Futures | 97.52-- |

| WTI Crude Oil | 63.58-- |

| Gold (COMEX) | 3668.00-- |

| US 10-Year Treasury Note Futures | 113.42-- |

| UK Long Gilt Futures (10Y) | 118.15-- |

| German Bund Futures (10Y) | 129.08-- |

| VIX Volatility Futures | 18.30-- |

| Italian BTP Futures (10Y) | 120.36-- |

| SONIA 3M Interest Rate Futures | 96.04-- |

| Copper (COMEX) | 4.61-- |

• Turkish TCMB Interest Rate Decision at 12:00 BST - Forecast: 41.0% vs Previous: 43.0% - Expected 200bp cut could signal shift in Turkey's aggressive tightening cycle and impact lira volatility.

• EU ECB Interest Rate Decision at 13:15 BST - Forecast: 2.15% vs Previous: 2.15% - Rate hold expected but focus on forward guidance amid eurozone growth concerns and potential divergence from Fed policy.

• EU Deposit Facility Rate at 13:15 BST - Forecast: 2.0% vs Previous: 2.0% - Key deposit rate likely unchanged with attention on ECB's easing bias and impact on euro money markets.

• US Core Inflation Rate MoM at 13:30 BST - Forecast: 0.3% vs Previous: 0.3% - Critical gauge of underlying price pressures that will influence Fed policy trajectory and dollar strength.

• US Inflation Rate YoY at 13:30 BST - Forecast: 2.9% vs Previous: 2.7% - Uptick in headline inflation could complicate Fed easing expectations and drive bond yields higher.

• US Core Inflation Rate YoY at 13:30 BST - Forecast: 3.1% vs Previous: 3.1% - Persistent core inflation above Fed target remains key obstacle to aggressive rate cuts.

• EU ECB Press Conference at 13:45 BST - Lagarde's commentary on growth outlook and policy stance will drive euro volatility and European equity direction.

• Adobe Inc. (ADBE) at 21:05 GMT [During-Hours] - Est: $5.18 vs Prev: $5.06 - Mega-cap software leader's results will signal enterprise spending trends and AI monetization progress across creative and document cloud segments.

• Kroger Company (KR) at 14:30 GMT [During-Hours] - Est: $0.99 vs Prev: $1.14 - Large-cap grocer's performance indicates consumer spending resilience and grocery inflation trends affecting broader retail sector sentiment.

• Empire Co Ltd Class A (EMP.A) at 11:30 GMT [Pre-Market] - Est: $0.63 vs Prev: $0.54 - Canadian food retailer's results may reflect North American consumer discretionary spending patterns and supply chain cost pressures.

• RH (RH) at 21:05 GMT [During-Hours] - Est: $3.21 vs Prev: $0.13 - Luxury home furnishing retailer's guidance will indicate high-end consumer demand and housing market health trends.

• Energean Plc (ENOG) at 13:00 GMT [Pre-Market] - Est: $0.56 vs Prev: N/A - UK-listed oil and gas producer's results will reflect European energy market dynamics and regional supply security developments.

• Fevertree Drinks PLC (FEVR) at 13:00 GMT [Pre-Market] - Est: $0.11 vs Prev: $0.05 - Premium mixer brand's performance indicates UK consumer discretionary spending and hospitality sector recovery trends.

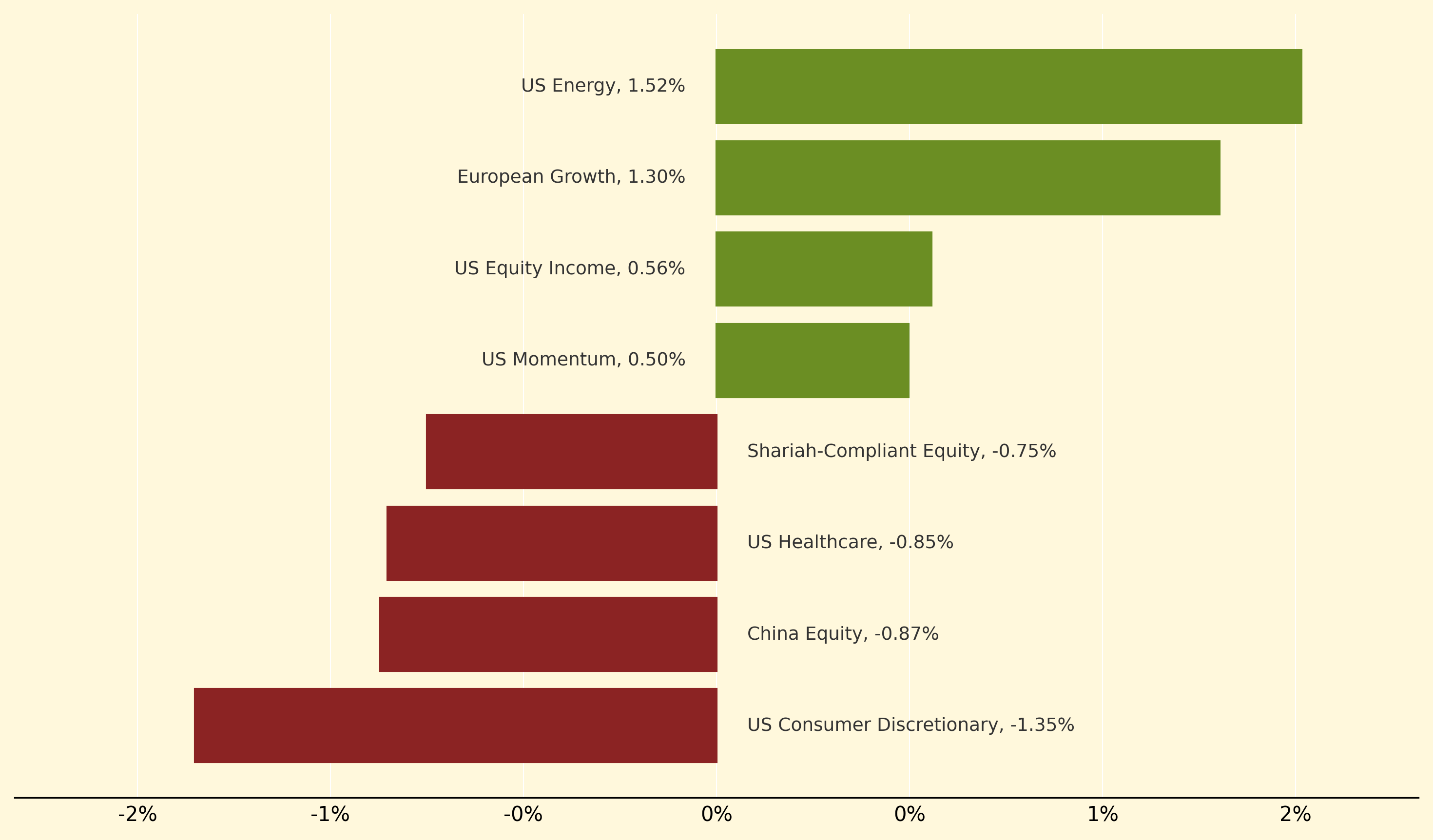

US Energy led the charge with a robust 1.52% gain as geopolitical tensions escalated, benefiting from oil's surge above $1 per barrel following Poland's downing of Russian drones. European Growth also performed strongly, advancing 1.3% amid broader market euphoria driven by the unexpected US producer price decline that stoked aggressive Fed rate cut expectations.

Conversely, US Consumer Discretionary underperformed significantly, dropping 1.35% as concerns about economic resilience and consumer spending weighed on sentiment. China Equity also lagged, falling 0.87% despite Beijing's consideration of a trillion-dollar local government debt relief package, reflecting persistent structural concerns about the world's second-largest economy.

Disinflationary: A gradual slowdown in the rate of price increases, where inflation declines but remains positive, signalling economic cooling without outright deflation. Markets typically react bullishly as it suggests central banks can ease monetary policy without triggering economic contraction or deflationary spirals.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry