US Court Invalidates Global Tariff Framework, Creating Policy Chaos | Links: [1], [2], [3]

A federal appeals court delivered a crushing blow to Trump's trade framework on Friday, ruling that most global tariffs, including the baseline 10% levy affecting multiple trading partners, were implemented unlawfully under emergency powers. The court's decision voids tariffs on consumer electronics, manufacturing inputs, and numerous sectors simultaneously, leaving trading partners "dazed and confused" according to officials briefed on the ruling. Whilst the court issued a stay until 14th October, creating a critical window for Supreme Court intervention, the decision injects profound uncertainty into global supply chain planning that companies have restructured around for years. Trump pledged to "win in the end" and escalate to the Supreme Court, but the ruling challenges fundamental executive trade powers.

Trump's Federal Reserve Challenge Undermines Monetary Policy Independence | Links: [4], [5], [6]

The US court appeal coincides with the Trump administration's unprecedented bid to dismiss Federal Reserve Governor Lisa Cook, escalating into a constitutional crisis over central bank independence. A hearing concluded Friday without ruling on Cook's removal, whilst Fed officials express growing concern about political interference in monetary policy. The implications extend far beyond personnel changes—Trump's broader ambitions to gain "control of the Federal Reserve board" would fundamentally alter the institution that anchors global monetary policy. Fed officials Daly and Waller already signal openness to September rate cuts, but these policy signals are now clouded by questions over institutional credibility. The confrontation has pushed investors toward their "red line" on Fed independence, with market participants increasingly pricing in political risk premiums around US monetary policy.

China Defies Global Manufacturing Slump with Unexpected Recovery | Links: [7], [8], [9]

Away from American policy chaos, Chinese manufacturing activity returned to expansion in August, with private sector PMI reaching its fastest pace in five months at 51.1, confounding expectations and bucking the broader Asian manufacturing contraction. This surprise turnaround contrasts sharply with five consecutive months of official PMI contraction and manufacturing weakness across Japan, South Korea, and broader Asia due to US tariff pressures. The recovery coincides with Chinese tech giants outpacing the Nasdaq 100, suggesting domestic stimulus measures and AI investment are gaining traction. However, structural challenges persist with property sales continuing to decline and steel inventories rising, indicating the recovery remains fragile. The divergence positions China as an outlier in Asian manufacturing trends, potentially offering relief for commodity demand despite broader global trade uncertainties.

Semiconductor Trade War Intensifies with US Equipment Restrictions | Links: [10]

Meanwhile, the US revoked semiconductor equipment authorisations for Samsung and SK Hynix operations in China, affecting $2bn in annual spending and escalating tech trade tensions beyond the courtroom challenges. This action coincides with Nvidia facing China-related headaches as Alibaba unveiled competing AI chip technology, highlighting the semiconductor supply chain's vulnerability to geopolitical pressures. The move represents a significant hardening of US technology export controls, moving beyond individual company sanctions to systematic restrictions on critical manufacturing capabilities. The timing alongside tariff court rulings creates a complex landscape where legal challenges to trade policy coexist with tightening technology controls, suggesting a multi-front approach to economic competition with China that transcends traditional trade measures.

Precious Metals Rally Signals Broad-Based Monetary Policy Pivot | Links: [11], [12], [13]

Against this backdrop of policy uncertainty, gold climbed to four-month highs whilst silver jumped to 2011 levels as September rate-cut momentum builds across global central banks. The precious metals advance reflects growing conviction that the Federal Reserve will deliver significant easing despite persistent core inflation reaching 2.9% in July, whilst ECB officials signal dovish flexibility with risks of inflation easing beyond targets. This coordinated monetary pivot comes as economists project slow US growth and stubborn inflation extending well into 2026, suggesting central banks prioritise growth support over inflation control. Copper's approach to $10,000/ton after four weeks of gains adds to the reflation narrative, with hedge funds boosting yuan strength bets past the key 7.0 level as markets position for a world where judicial challenges reshape trade policy whilst monetary accommodation accelerates.

• EU Inflation Rate YoY Flash (Tuesday, 10:00 BST) - Previous: 2.0% - Key ECB policy indicator that will influence rate cut expectations and euro direction.

• US ISM Manufacturing PMI (Tuesday, 15:00 BST) - Previous: 48.0 - Critical gauge of US industrial health; reading above 50 would signal manufacturing recovery.

• AU GDP Growth Rate QoQ (Wednesday, 02:30 BST) - Previous: 0.2% - RBA policy implications as central bank weighs growth versus inflation pressures.

• US JOLTs Job Openings (Wednesday, 15:00 BST) - Previous: 7.437M - Fed's preferred labour market metric ahead of Friday's payrolls data.

• AU Balance of Trade (Thursday, 02:30 BST) - Previous: A$5.365B - Commodity export strength indicator affecting AUD and resource sector sentiment.

• CA Balance of Trade (Thursday, 13:30 BST) - Previous: C$-5.86B - Bank of Canada policy consideration as trade performance impacts growth outlook.

• US ISM Services PMI (Thursday, 15:00 BST) - Previous: 50.1 - Services sector dominance makes this crucial for Fed policy as economy teeters near contraction.

• GB Retail Sales MoM (Friday, 07:00 BST) - Forecast: 0.5% vs Previous: 0.9% - Consumer spending strength will influence BoE rate cut timing expectations.

• CA Unemployment Rate (Friday, 13:30 BST) - Previous: 6.9% - Bank of Canada closely monitoring labour market for aggressive easing signals.

• US Non Farm Payrolls (Friday, 13:30 BST) - Previous: 73K - Critical Fed input with weak reading potentially accelerating September rate cut expectations.

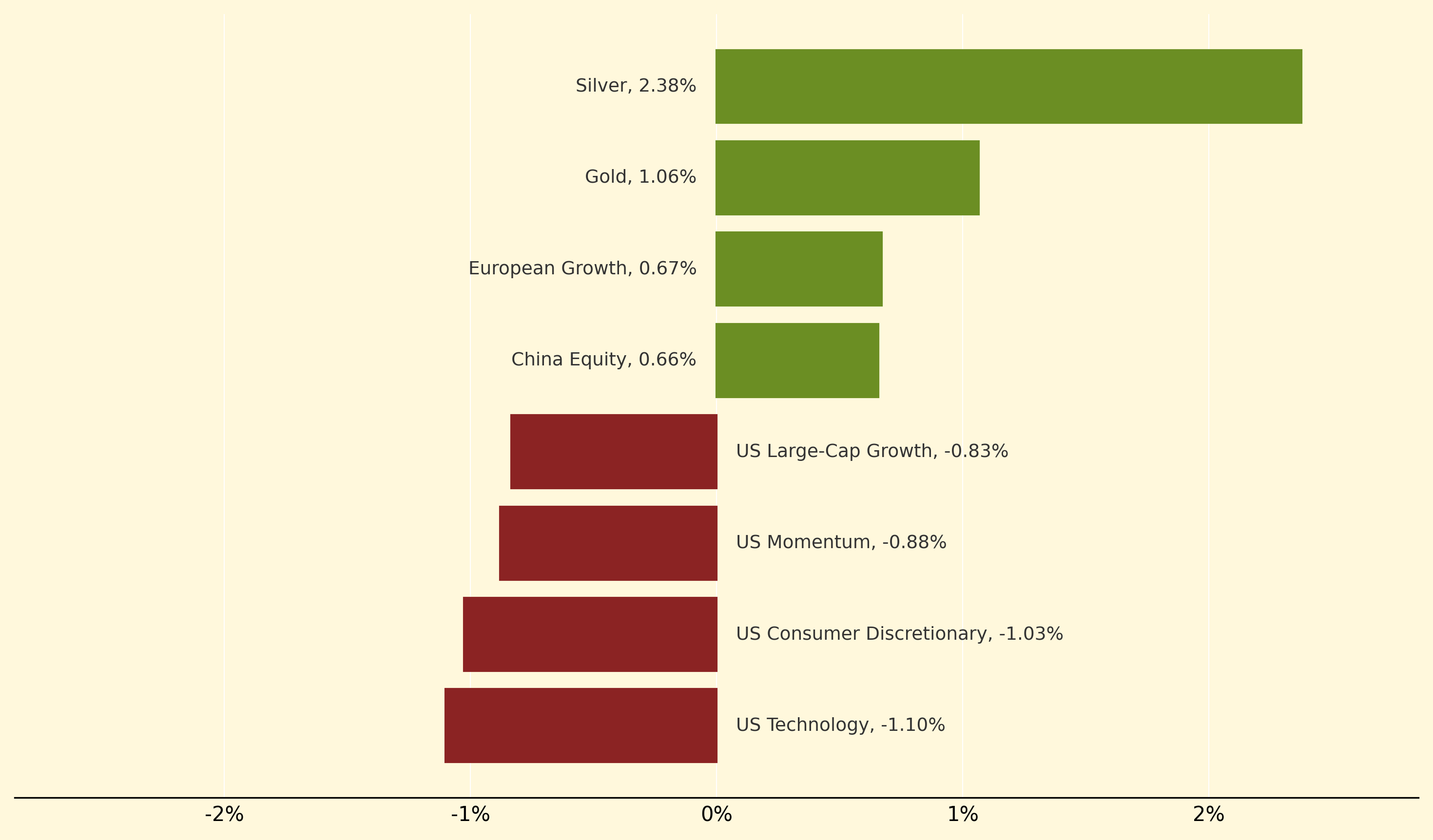

Silver jumped 2.38% and Gold advanced 1.06% as precious metals capitalised on mounting September rate-cut momentum and policy uncertainty from the tariff court ruling. European Growth (+0.67%) and China Equity (+0.66%) also posted solid gains, with Chinese strategies benefiting from unexpected manufacturing PMI expansion to 51.1, defying broader Asian contraction trends.

Conversely, US Technology fell 1.10% and US Consumer Discretionary dropped 1.03% as semiconductor restrictions on Samsung and SK Hynix operations in China intensified tech sector pressures. US Momentum (-0.88%) and US Large-Cap Growth (-0.83%) also declined amid broader concerns over Fed independence challenges and the appeals court's invalidation of global tariffs creating policy chaos for growth-oriented strategies.

Emergency powers overreach: Legal doctrine restricting presidents from using extraordinary authorities like the International Emergency Economic Powers Act to implement broad economic policies during non-crisis periods, as demonstrated by the court's invalidation of Trump's global tariff framework.

Thanks for reading Morning Fill. Have a great day!

Ollie and Harry